Personal Story · 6 min read

I had a number in my head. My “real” monthly expenses. The number I’d been telling myself — and my partner, and anyone who asked — was somewhere around $2,400. Rent, car, food, utilities. I’d done the math in my head. It felt right.

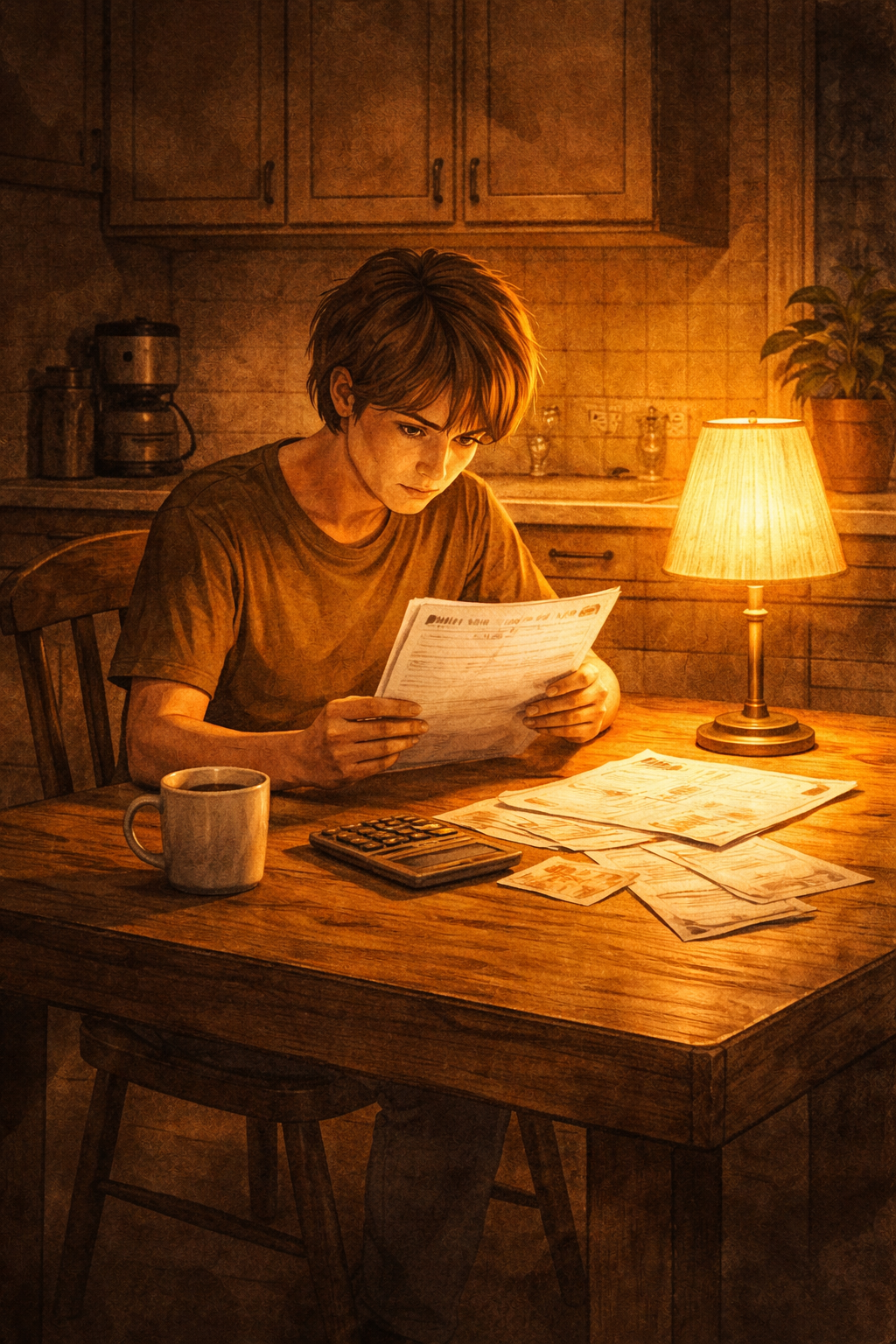

Then one February afternoon, because I was genuinely scared about why my bank account kept hitting zero, I sat down with three months of bank statements and actually added it up.

The real number was $3,190.

I’d been off by $790 a month. Every month. For at least a year.

The lies we tell ourselves about money

It wasn’t one big lie. It was twenty small ones.

The $17 Netflix I hadn’t counted because it “barely counts.” The $65 meal kit subscription I’d forgotten was still running. The $35 gym membership I told myself I’d cancel “next month” for six consecutive months. The $12 news site I signed up for during an election and never turned off. The Spotify, the cloud storage, the parking app with the monthly fee I didn’t know about until I looked. Small things. Each one invisible on its own.

And the grocery estimate. I’d been telling myself $300/month on groceries. The actual number, averaged across the three months I looked at, was $428. I wasn’t buying luxury food. I was buying the same things I always bought — I’d just never actually counted.

The gap between my mental budget and my real spending wasn’t laziness or recklessness. It was comfortable vagueness. The vagueness felt safe. As long as I didn’t look at the exact number, I could maintain the fiction that I was roughly okay.

What looking at the actual number felt like

Uncomfortable. Really uncomfortable. Not in a crisis way — in the way it feels when you’ve been avoiding something and you stop avoiding it. There was a moment where I wanted to close the spreadsheet and tell myself it was probably a weird month.

I didn’t. I checked another month. Same pattern.

And then something shifted. Because now I had a real problem instead of a vague anxiety. A real problem has a size. It has edges. You can look at it and say: this is the thing I’m dealing with, and here are the specific things I could do about it.

Vague financial anxiety doesn’t work that way. It’s everywhere and nowhere. It follows you to sleep and wakes up with you. A $790 gap is specific. It’s uncomfortable, but it’s solvable.

What I actually did

The first thing I did was cancel everything I hadn’t actively decided to keep that month. The meal kit, the gym I wasn’t using, the extra streaming service I’d forgotten about. That closed about $130 of the gap in ten minutes.

The second thing was accepting that my grocery estimate was wrong and rebuilding the budget from the real number. That sounds simple. It wasn’t emotionally simple. Admitting that I’d been wrong — not guessing, not approximating, but genuinely wrong — required me to stop defending the old number and just let it go.

The third thing was the hardest: I told my partner. Not in a “we’re in crisis” way, but in a “I looked at this honestly and here’s what I found” way. That conversation was terrifying to start and relieving to finish.

Over the next three months, the gap closed. Not all at once. Not perfectly. But it closed. And more importantly, I stopped lying to myself — not because I became a more virtuous person, but because I’d seen what comfortable vagueness was actually costing me.

The thing no budgeting guide tells you

The technical part of budgeting — the categories, the percentages, the apps, the spreadsheets — is the easy part. The hard part is the moment before the math, when you have to decide to look at the real number instead of the comfortable approximation.

That moment is a choice. And it’s a choice you make over and over, not just once. Every month is a small version of that February afternoon: will I look at what actually happened, or will I stay in the comfortable vagueness?

I still choose vagueness sometimes. Probably more than I’d like to admit. But I choose it less than I used to. And the gap between my mental number and my real number keeps getting smaller. Not because I’m better at math. Because I’m less afraid of the actual answer.

If you’re not sure where to start

Pull up three months of bank statements. Add up what you actually spent — not what you think you spent. Write it down. If the number surprises you, that’s the work. Not the categories, not the apps, not the system. The willingness to look at the real number and not flinch.

That’s where it starts.

Keep building

Your First Budget in 30 Minutes · America’s Credit Card Crisis: What It Means for You · What Is Net Worth and Why It Matters

Leave a Reply