Municipal bonds experienced fluctuations in certain areas as the week’s final major releases unfolded, with municipal bond mutual fund flows demonstrating retail participation and high-yield bonds consistently outperforming the broader investment-grade market. Uncertainties surrounding inflation expectations and potential rate cut timings prompted pressure on U.S. Treasuries, as economic data and Federal Reserve statements gave market players pause. Equities concluded the session with losses, further contributing to the turbulent market environment.

Yield Movements and Ratios

Triple-A yields observed a slight increase of one to two basis points, while Treasury yields surged by up to six basis points at the close of trading. Refinitiv Municipal Market Data indicated various muni-to-Treasury ratios, with figures such as 65% for the two-year term, 63% for the five-year term, and 83% for the 30-year term. These ratios provide insight into the relative performance of municipal bonds compared to Treasury securities at different maturity points.

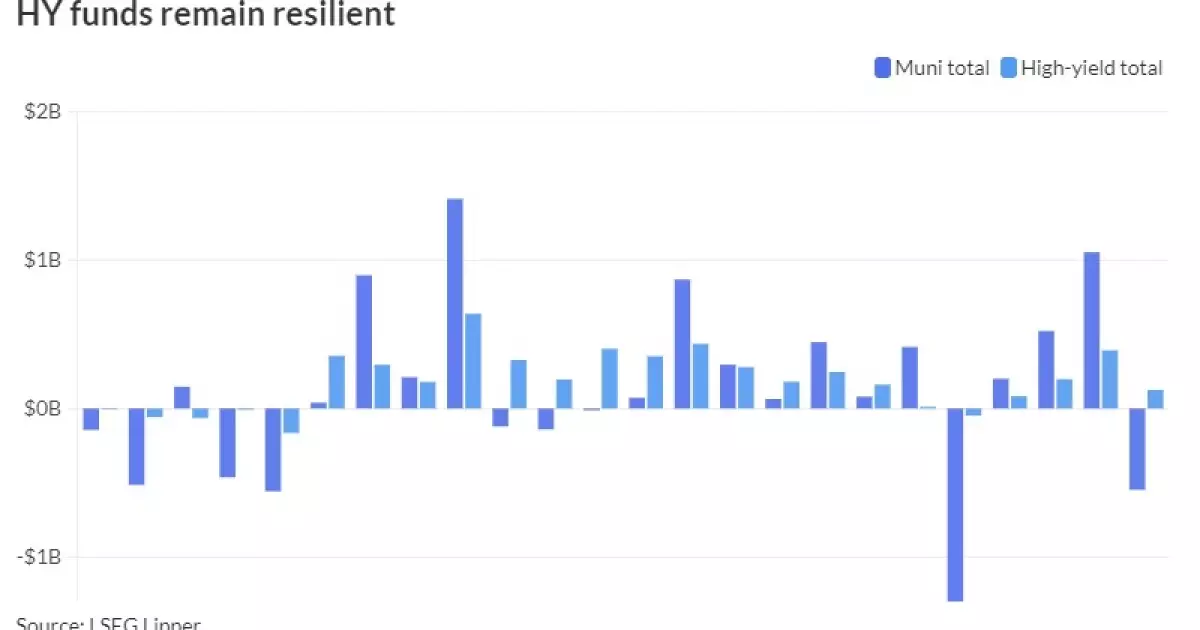

Despite high-yield municipal bond funds attracting inflows of $125 million, municipal bond mutual funds experienced outflows of $548 million according to LSEG Lipper data. J.P. Morgan’s Peter DeGroot highlighted the resilience of high-yield funds in terms of credit quality, contrasting them with the outflows of $673 million witnessed by investment-grade funds. Notably, the rise of exchange-traded fund (ETF) inflows by $91 million partially offset the outflows from open-end funds, underscoring the increased engagement of retail investors in recent weeks.

The recent market trends have shown a divergence between municipal bonds and U.S. Treasuries, with municipal bonds exhibiting slight weakness compared to the robust run observed by Treasuries. Kim Olsan of FHN Financial attributed this underperformance to the substantial issuance levels and relative value considerations. As the Bond Buyer 30-day visible supply reached $16.55 billion, Olsan noted that such a significant supply often indicates the availability of a wide range of credits on the market, leading to adjustments in yield ratios. This influx of new issues, particularly in the lower-rated segment, has contributed to the high-yield outperformance trend.

Credit Quality and Yield Spreads

The disparity in new issuance has driven credit spreads wider across various credit segments, with higher-grade names dominating the market. Olsan emphasized the attractive levels at which in-demand New York credits were priced, citing yields of over 6% for certain issues. Moreover, the customer-buy volume revealed by MSRB data indicated strong interest in specific yield buckets and credit ranges, suggesting the discerning behavior of investors in the current market landscape.

Refinitiv MMD, ICE, S&P Global Market Intelligence, and Bloomberg BVAL reported subtle shifts in AAA yield curves, reflecting the evolving pricing dynamics across different maturity points. U.S. Treasuries experienced weakening, with various maturity yields increasing marginally. These yield movements, alongside the broader market performance trends, underscore the complex interplay of economic data, investor behavior, and supply dynamics that shape the municipal bond landscape.

The current municipal bond market exhibits a mix of strengths and weaknesses, influenced by a myriad of factors ranging from credit quality preferences to yield spread considerations. The interlocking relationships between issuance levels, investor sentiment, and economic indicators create a dynamic environment that demands careful observation and strategic decision-making from market participants. By staying attuned to these evolving trends and understanding the underlying drivers, investors can navigate the municipal bond market with greater confidence and effectiveness.