The municipal bond market has shown little change in recent days, with U.S. Treasuries being firmer and equities experiencing mixed activity towards the end of the session. Despite this stability, municipal bond yields remain consistent with levels observed at the beginning of the summer last year. According to Tom Kozlik, the managing director and head of public policy and municipal strategy at HilltopSecurities, there is a possibility of yields moving even lower in the future, particularly after the Federal Reserve communicates its intentions to ease policy in upcoming meetings.

Municipal bonds are displaying signs of positive momentum with stronger mutual fund inflows and consistent demand from separately managed accounts. Despite the solid pace of tax-exempt issuance, yields are falling, and the market remains optimistic. The issuance of municipal bonds has reached $277.228 billion year-to-date, marking a 3.13% increase compared to the previous year. As August approaches, issuance is expected to slow down as market participants take summer breaks. Additionally, the upcoming November election is anticipated to contribute to lighter supply, preventing significant changes in muni paper pricing.

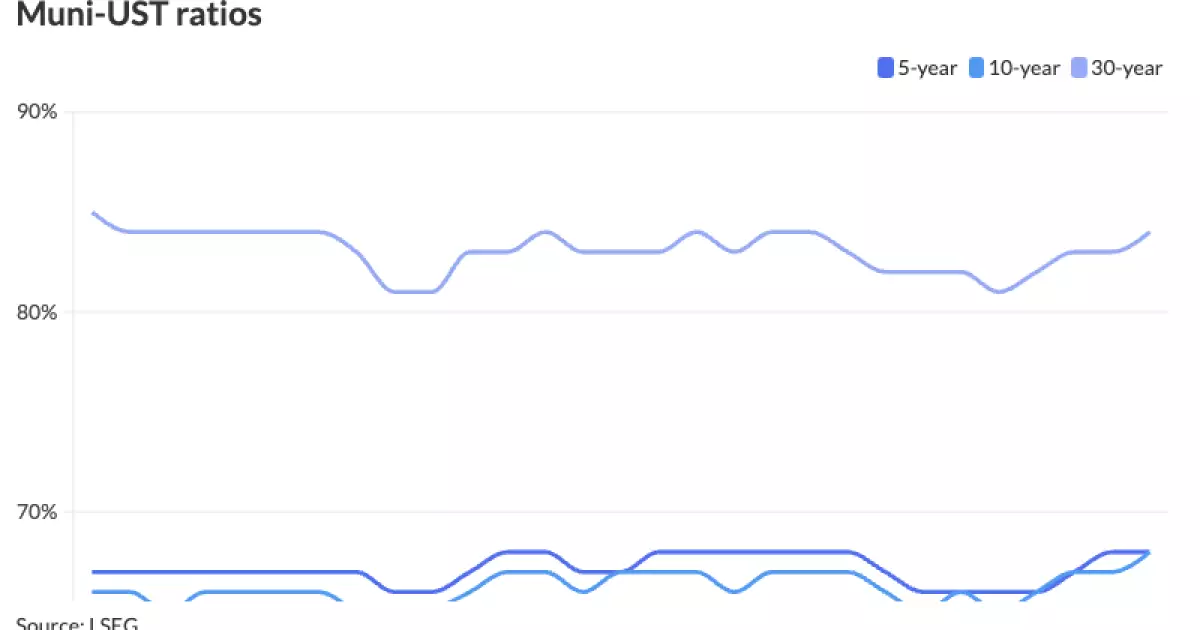

The muni-to-Treasury ratios indicate that buying opportunities may not be as attractive as desired by investors. The demand for munis is strongest in institutional muni funds, although deep and consistent demand from 2021 is still lacking. Chris Brigati, senior vice president and director of strategic planning and fixed-income research at SWBC, suggests that the next phase of demand could accelerate as rate easing expectations grow. With the current market conditions, tax-exempt municipals are becoming increasingly favorable.

Recent trends show steady reinvestment funds for SMA portfolios, while inflows into muni mutual funds and exchange-traded funds have been on the rise. Retail muni allocations are expected to benefit from recent equity price volatility. August marks the last major surge of reinvestment dollars in 2024, presenting both opportunities and challenges for the municipal bond sector. The sector will need to maintain SMA buyer interest in the face of shrinking yields and available income due to fund inflows or potential rallies following the Fed meeting or jobs data release.

In the primary market, several significant bond issuances took place recently. Wells Fargo priced $1.105 billion of GOs for New York City, while BofA Securities and J.P. Morgan priced bonds for the Port of Portland, Industrial Development Authority of Fairfax County, Central Florida Expressway Authority, and Illinois Housing Development Authority. These offerings indicate the continued activity and interest in municipal bonds, despite the challenges posed by the current market conditions.

The municipal bond market is expected to see ongoing activity, with issuances and trading remaining steady. The impact of future policy decisions by the Federal Reserve, as well as economic indicators such as job data and equity market performance, will play a significant role in shaping the direction of the market. Investors and market participants will need to closely monitor these factors to make informed decisions regarding municipal bond investments.