The Federal Reserve, as the central bank of the United States, plays a critical role in shaping the economic landscape through its monetary policy actions, particularly interest rate adjustments. As we approach December 18, a significant decision looms on the horizon: the potential for another quarter-point reduction in interest rates. If enacted, this would represent the third consecutive cut, cumulatively lowering the federal funds rate by one percentage point since September. This trend towards easing comes in response to a historically high inflation rate, prompting the Fed to recalibrate its policies after a phase of aggressive rate hikes.

The federal funds rate, essentially the rate at which banks lend to one another on an overnight basis, holds substantial influence over consumer borrowing costs. Although consumers do not pay this exact rate, it serves as a benchmark that affects various interest rates that consumers engage with daily. A reduction on December 18 would adjust the overnight rate down to a range of 4.25% to 4.50%, creating a ripple effect across different borrowing categories. Economic observers are weighing the potential outcomes of this forthcoming decision—could it alleviate some financial pressure on consumers?

While expectations point toward an immediate easing, analysts caution that this might not be a comprehensive solution to consumer financial burdens. Jacob Channel, a senior analyst, opines that we might witness a “wait-and-see” approach following this cut, especially considering the impending uncertainties surrounding President Joe Biden’s fiscal policy as he embarks on the second year of his term. The critical question remains: will the timing of these cuts effectively match the economic realities faced by borrowers?

Consumer borrowing costs are a significant area of concern, particularly in the aftermath of high interest rates. Credit cards, car loans, and mortgages are among the key areas where changes are closely monitored. For instance, credit cards often have variable interest rates, directly tied to movements in the Fed’s benchmark. Since interest rates have surged from 16.34% in March 2022 to a staggering 20.25% today, consumers have seen the mounting pressure of these costs. Despite recent Fed cuts aimed at reducing these burdens, lenders typically adjust their rates slowly, leading analysts like Greg McBride to suggest that those carrying credit card debt consider alternatives like balance transfers instead of waiting for rate adjustments.

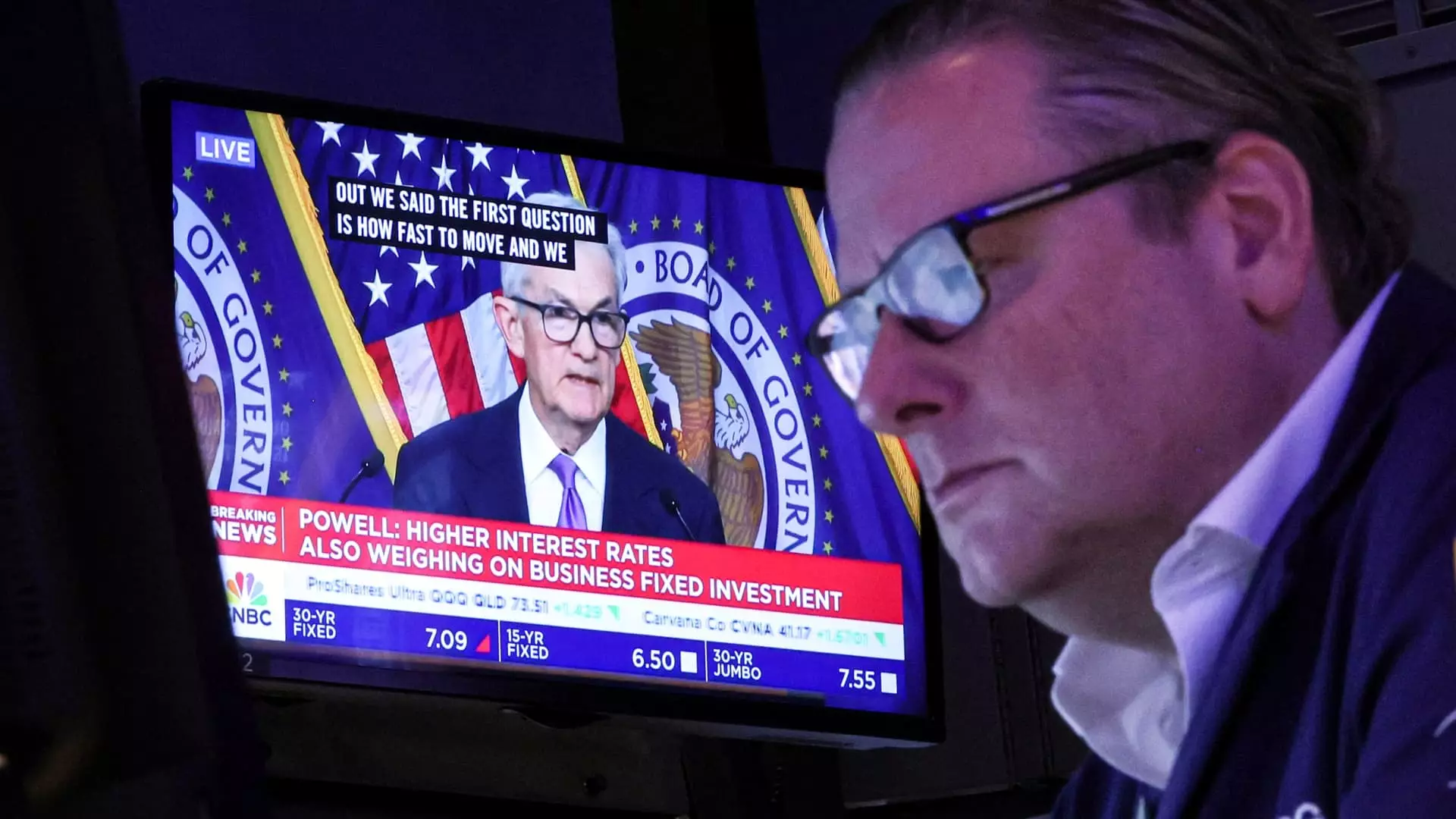

Mortgage rates present a different challenge, as fixed-rate mortgages are primarily influenced by Treasury yields and overall economic conditions rather than directly responsive to Fed rate cuts. For those financing homes under fixed-rate mortgages, significant changes in monthly payments won’t occur until refinancing becomes necessary. The current average mortgage rate stood at 6.67% as of early December, which, despite being lower than the previous month, lingers above earlier lows in 2024. Analysts predict a continuing ebb and flow in mortgage rates, complicating the decision for potential homebuyers.

Similarly, the auto loan market reflects the broader trends in consumer borrowing. While rates remain fixed, rising vehicle prices are resulting in larger loan amounts, putting pressure on budgets. With the average new car loan rate around 7.59%, potential buyers find themselves confronted with high costs that are not alleviated by the anticipated Fed cuts. As McBride highlights, even significantly lower rates may not cushion the financial strain from inflated car prices, leaving consumers with sizable monthly payments.

Meanwhile, the student loan sector varies considerably in response to shifts in the federal funds rate. Fixed-rate federal student loans remain untouched by immediate rate cuts, but borrowers with private student loans that are linked to fluctuating indices may benefit as rates decrease. Yet, the complexities of refinancing remain, requiring borrowers to consider the potential loss of protective measures that federal loans offer.

The Federal Reserve’s anticipated interest rate cuts present a mixed bag of implications for consumers. While psychological relief may arise from these decisions, the tangible financial benefits may dissipate as other economic pressures persist. As the economy navigates uncertain waters, it becomes increasingly essential for consumers to remain informed, exploring strategies to manage their debts effectively in light of fluctuating interest rates. The interplay between monetary policy and its real-world effects remains intricate, highlighting the importance of strategic financial planning in a landscape marked by uncertainty.