As the financial environment shifts under the pressures of increasing interest rates and fluctuating market conditions, the dynamics surrounding Build America Bonds (BABs) have noticeably changed. Specifically, recent trends indicate a deceleration in the redemptions of these bonds, despite some issuers expressing intentions to call back their BABs by year-end. Analysis reveals that, as of 2024, approximately $14.9 billion of BABs have already been refunded, with an additional $938.3 million poised for redemption according to J.P. Morgan’s latest figures. Interestingly, a total of 39 issuers have pursued refinancing options for their outstanding BABs this year, illustrating a complex interplay between market conditions and issuer decisions.

The decision to refinance existing BABs hinges on economic rationale, primarily driven by interest rate comparisons. Nick Venditti, head of Municipal Fixed Income at Allspring, points out that issuers will only pursue refunds if there’s a tangible economic benefit, most prominently when interest rates are substantially lower. With the current 10-year U.S. Treasury note yielding 4.27% and municipal bonds experiencing a selloff, potential savings from BAB redemption are now more elusive. The early months of 2024 witnessed sluggish activities in BAB refundings, a pattern that shifted dramatically in Q2, only to taper off again in the subsequent quarter.

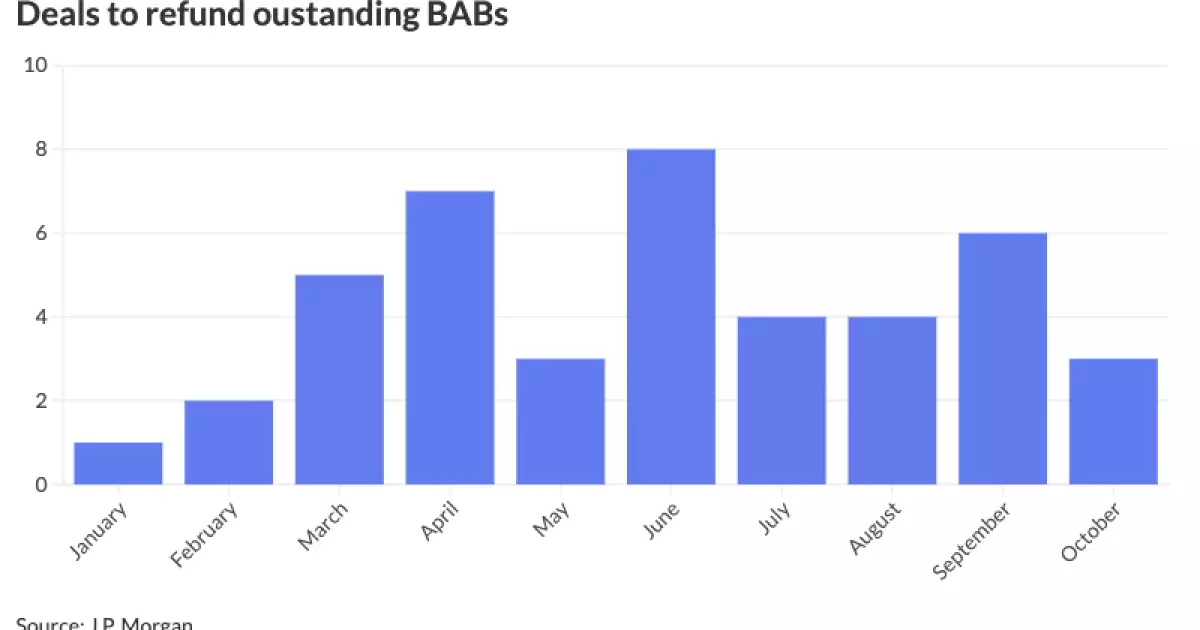

June marked a peak in BAB refinancing activity, with eight transactions taking place, indicating a robust response to favorable market timing. This was closely followed by April, which recorded seven deals, whereas January lagged significantly with only a single transaction. These fluctuations in market participation reveal the careful timing required by issuers in navigating the choppy waters of bond markets, affecting their decisions on whether to proceed with refinancing.

The trepidation over rising interest rates has tempered demand for BAB refundings, a sentiment echoed by industry experts. James Pruskowski, chief investment officer at 16Rock Asset Management, indicates that a lackluster performance from the municipal market during Q3 has diminished the urgency for refinancing among issuers. After a burst of activity in the second quarter, subsequent inaction underscores the cautious nature adopted by many stakeholders in light of new market realities.

Additional commentary from Barclays strategist Mikhail Foux points out that as municipal-UST ratios ascend, the motivation for issuers to utilize extraordinary redemption provisions (ERPs) in BAB refundings is likely to decrease further. Higher ratios often emerge during periods where tax-exempt bonds struggle, complicating the cost-benefit calculations that issuers need to make regarding their BAB portfolios.

Market volatility has further compounded challenges for those looking to refund BABs. A specific case arises from the Ohio Water Development Authority, which recently opted to withdraw its planned $102.02 million refinancing deal due to uncertainty in the market conditions. Remarkably, the authority’s executive director, Mike Fraizer, articulated that potential net present value savings had drastically diminished, prompting a strategic pause until the market stabilizes.

Despite the surrounding volatility, some entities, such as the Regents of the University of California, have proceeded confidently with their plans, highlighting a notable divergence in issuer sentiment. This uneven response showcases the varied impacts of market fluctuations on individual issuers, exacerbated by recent controversial legal challenges that have influenced their decision-making processes.

From an investor perspective, current market dynamics have rendered outstanding BABs significantly less appealing. As highlighted by Venditti, the call risk associated with these bonds has dissuaded many institutional investors, particularly insurance companies looking to align assets and liabilities. Traditional BABs are now viewed as highly undesirable investment instruments, leading to a scenario where they may be considered “almost uninvestable” without solid legislative assurances regarding their redemption structures.

The obstacles faced by Build America Bonds amidst shifting market conditions are multifaceted, encompassing economic, regulatory, and sentiment-based factors. As issuers navigate through rising interest rates and market volatility, the outlook for BAB refundings remains uncertain, requiring a careful recalibration of expectations for both issuers and investors alike. The tension between short-term market fluctuations and long-term strategic objectives will undoubtedly shape the future landscape of BABs, continuing to present significant challenges and opportunities.