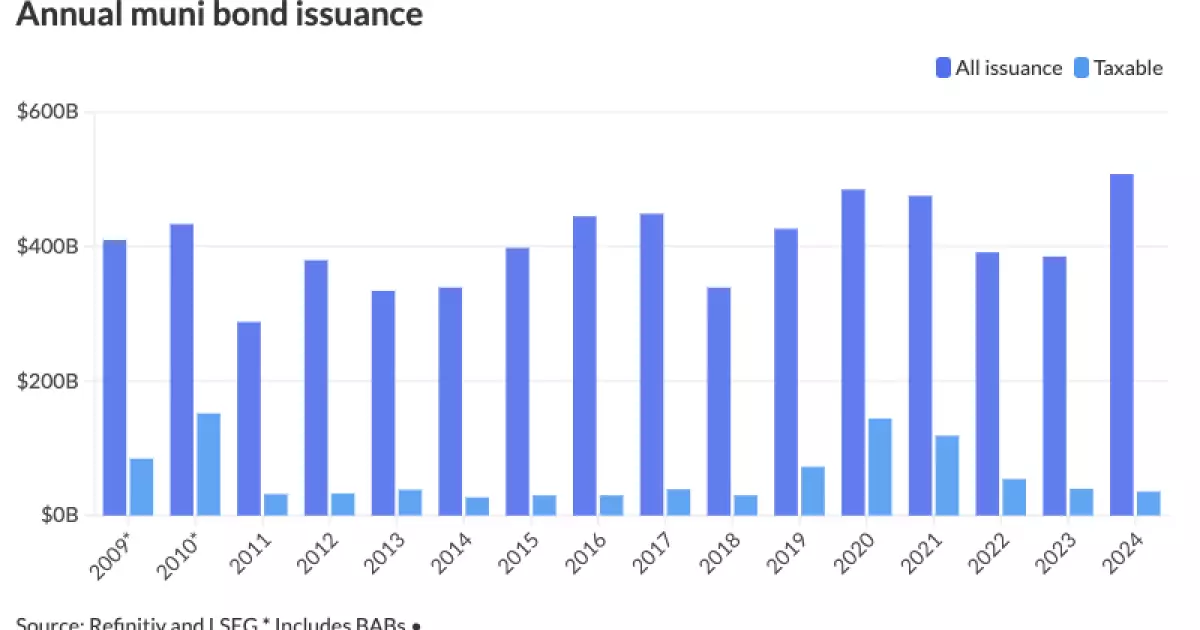

The year 2024 has been a remarkable one for the municipal bond market, witnessing an issuance surge that saw total debt climb above the $500 billion mark. This unprecedented figure, estimated at approximately $507.585 billion, reflects a substantial growth of 31.8% from $385.061 billion in 2023, shattering the previous record of $484.601 billion set in 2020. The driving forces behind this dramatic increase are multifaceted, but consensus points to a combination of heightened infrastructure spending needs, strategic responses to election-related uncertainties, and a slew of mega deals that prompted issuers to flood the market.

The landscape of the municipal bond market is particularly interesting as different segments exhibit varying trends. Tax-exempt issuance soared by 36% to $446.673 billion, while taxable issuance saw a decline of 10.5% to $35.632 billion. Notably, refunding activities surged by an impressive 63.6% to $84.479 billion, indicating a significant reassessment among issuers regarding outstanding debt obligations. The new-money volume, used for fresh projects, also displayed robust growth, climbing 19% to $355.607 billion.

Reflecting on the year’s trends, analysts initially forecasted a range for issuance that varied considerably—from a low of $330 billion to a high of $450 billion. These projections were shaped by diverse factors including the winding down of pandemic-era federal aid, pent-up demands, inflationary pressures, Federal Reserve monetary policies, and of course, the looming 2024 elections. However, as the year unfolded, it became apparent that the market was on track for a more significant upswing than anticipated.

As market participants recalibrated their expectations, revised forecasts indicated a more narrowly defined range between $385 billion and $460 billion. The ability of the market to adapt to changing conditions, including the acceptance of higher yield rates, allowed issuers to capitalize on favorable circumstances to issue bonds more aggressively. Kim Olsan from NewSquare Capital illustrated this phenomenon by suggesting that the year could be framed as a “Goldilocks year,” where buyers benefited from higher yields while issuers found favorable conditions for bringing new deals to market.

One key contributor to this record issuance was the urgent need for infrastructure upgrades fueled by diminishing federal aid. Following significant stimulus packages in 2021 and 2022, municipalities initially sought to conserve cash reserves, minimizing the need to issue bonds. However, as those financial supports waned, the existing infrastructure demands became increasingly pressing.

Chris Brigati, chief investment officer of SWBC, emphasized the growing infrastructure needs stemming from urban sprawl and population growth across various regions, particularly in the Southwest and Southeast. The critical need for new highways, hospitals, schools, and other civic amenities has created a scenario where issuers can no longer avoid tapping into the bond market to finance these essential projects.

The latter half of 2024 saw a notable uptick in mega deals—bond issues exceeding $1 billion—which have become more commonplace and well-received. Olsan noted that liquidity in these larger transactions attracted a broader base of buyers, providing issuers with the confidence to pursue ambitious financing strategies without fear of adverse market reactions.

Moreover, the timing of the presidential elections influenced municipal bond issuance activity. Historically, significant issuance volumes tend to spike preceding elections, as issuers strive to mitigate any associated market volatility. The pattern observed in October 2024, with a record issuance of $64.643 billion, echoed similar past cycles, underscoring how political seasons shape bond markets.

As we anticipate 2025, projections suggest that issuance could see a further increase, with estimates ranging from $480 billion to an astonishing $745 billion. Factors contributing to these forthcoming trends include potential shifts in tax policy, macroeconomic conditions related to interest rates, and anticipation of future federal aid. Therefore, analysts expect next year’s issuance may closely align with or surpass 2024’s historic highs.

However, uncertainty remains as potential tax policy adjustments loom on the horizon. Issuers might proactively flood the market to capitalize on existing tax exemptions before any legislative reforms take effect, spurred by the need to fill the funding gaps left by the expiration of previous tax acts.

November and December issuance numbers further highlighted regional disparities. California emerged as the leader in issuance, contributing $71.601 billion, followed closely by Texas and New York. Florida showcased remarkable growth by more than 100%, while other states also experienced varying degrees of increases.

2024 has proven to be an extraordinary year for the municipal bond market, not just in terms of issuance volumes but also in how issuers and investors navigated complex economic landscapes. The prospects for 2025 remain dynamic and will require keen observation as the political and fiscal environments continue to evolve.