As tax season is currently in full swing, the municipal bond market is experiencing some underperformance and pressure from investors looking to liquidate short-term paper to meet their tax obligations. The muni market has seen negative returns of 0.06% for the month, while U.S. Treasuries are up by 0.63% and corporates have gained 1.18%. According to Bloomberg data, the one-year index shows negative returns of 0.04% so far in March and positive returns of 0.08% for 2024. Market experts like Steve McLaughlin from S&P Global Market Intelligence have acknowledged that munis typically underperform during this time of the year due to anticipated selling to cover tax liabilities. Jeff Lipton, managing director of credit research at Oppenheimer Inc., mentioned that tax loss harvesting at the end of the previous year may result in substantial tax bills for investors.

During tax season, investors tend to sell off their municipal bonds, leading to wider spreads and higher yields. This is especially noticeable in the front end of the curve where more selling occurs. Wesly Pate, senior portfolio manager at Income Research + Management, highlighted that investors holding assets to make tax payments usually opt for short-duration or variable-rate demand notes. Municipal Securities Rulemaking Board data shows an increase in flows for one-year and in paper, indicating market participants are utilizing municipal front-end paper to settle tax liabilities. Short-duration investors often face funding pressures during tax season, causing significant market volatility. As a result, fund managers prepare by building up liquidity in anticipation of outflows.

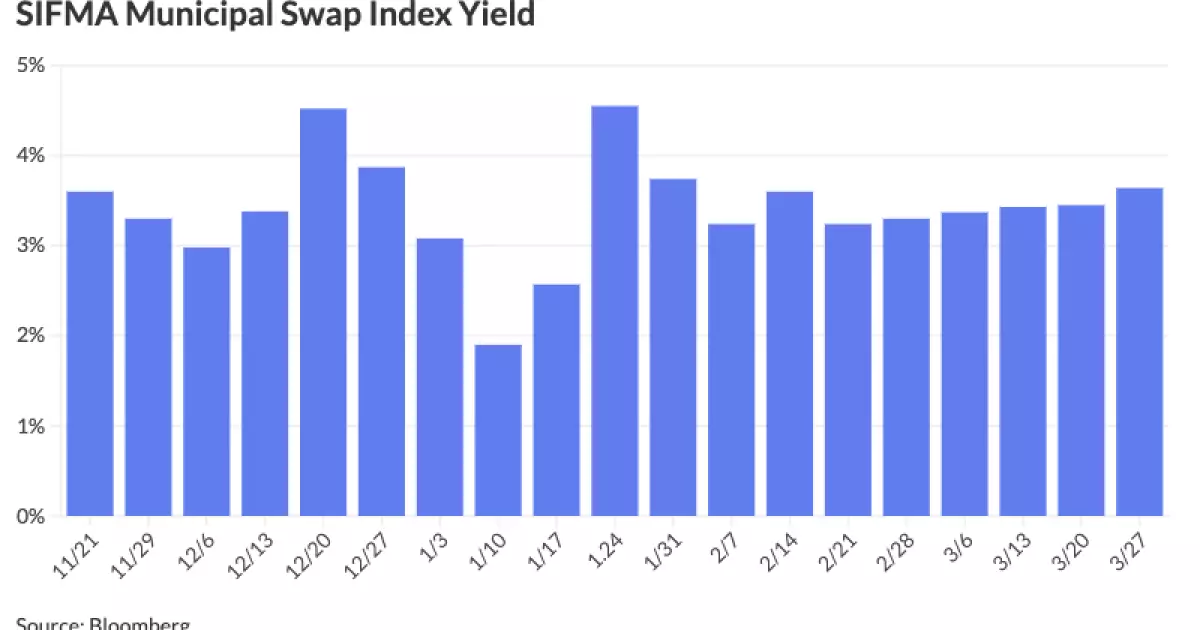

Short-term mutual funds have witnessed small outflows in recent weeks, with investors seeking low or limited duration assets to carry them through tax season without significant risk. The demand for variable-rate demand notes (VRDNs) has increased as high-net-worth individuals look for options with shorter durations but some yield. The expected money-fund redemptions are pressuring floating-rate yields, leading to fluctuations in fixed maturity ranges. Market participants anticipate a seasonal increase in SIFMA resets as tax season approaches, although the increase is expected to be tempered due to the delicate supply-demand balance in the market.

Historically, tax-exempt money market funds see outflows before Tax Day, causing SIFMA to cheapen, which usually corrects itself post-Tax Day when flows reverse. Despite the tax season selling pressure, market experts believe that there will be less volatility this year due to the healthy supply in the market that can absorb the selling. The ongoing structural mismatch between new-issue supply and strong investor demand has kept yield volatility well contained. Market participants predict a renewed interest in munis across the curve following tax payments, as investors seek tax havens. The inflows into muni mutual funds and separately managed accounts suggest a favorable entry point for new buyers in the market.

Tax season has a noticeable impact on the dynamics of the municipal bond market, with investors adjusting their portfolios to meet their tax obligations. While the market experiences some underperformance and selling pressure during this period, the overall demand for munis remains strong, signaling a positive outlook for the asset class beyond the short-term fluctuations caused by tax season.