On Thursday, municipal bonds exhibited a solid performance, maintaining stability amidst the fluctuations seen in other markets. As some of the most significant deals of the week reached their pricing milestones, municipal bond mutual funds saw inflows for the 13th consecutive week, driven significantly by high-yield bonds. This resilience marks a clear separation from the mixed sentiments dominating the U.S. Treasury landscape, where equities managed to rally, leaving munis on their own definitive upward trajectory.

The ratios between municipal bonds and U.S. Treasuries reveal important insights into market behavior. As of 3 p.m. EST on Thursday, the two-year muni-to-Treasury ratio stood at 64%, with similar figures for the three-year and five-year at 64% and 65%, respectively. The ten-year ratio crawled to 69%, with the thirty-year reaching a noteworthy 85%. This consistent data provided by Refinitiv Municipal Market Data reflects a market that, although steady, is demonstrating significant investor confidence and an underlying demand for quality bonds among consumers.

Despite the robust issuance volume, a notable gap appears between supply and demand according to Kim Olsan, a senior fixed income portfolio manager at NewSquare Capital. The volume of “daily bids wanted” during September has dropped considerably, at 15% lower compared to the average. Originally expected issuance this month surpasses $40 billion, marking a surge against the preceding decade’s average of approximately $34 billion. The Bond Buyer’s current visible supply is listed at around $13.98 billion, a significant figure reflecting heightened market activity.

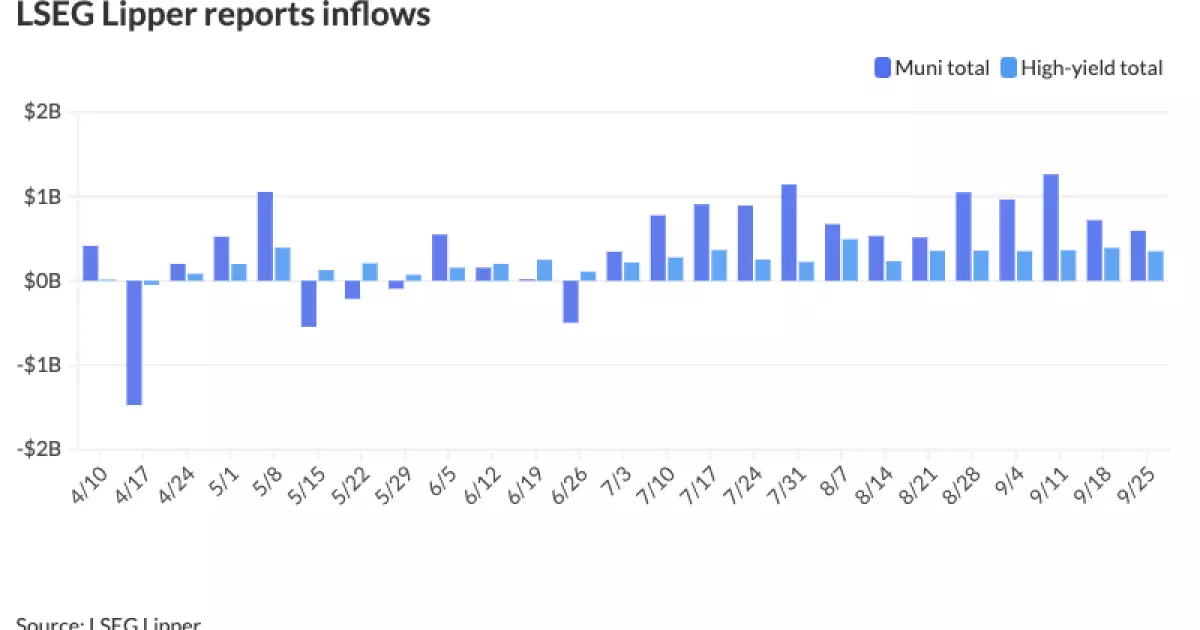

Moreover, the supportive nature of mutual fund inflow data illustrates how well investors are responding to the market’s current signals. This quarter alone has seen net inflows of $8.8 billion, with a paltry single week showing nominal outflows. Data from LSEG Lipper indicates a surge of $592.1 million into funds for the week ending Wednesday, following $718.4 million the week prior, establishing 13 weeks of consistent inflows. The persistent interest in high-yield solutions remains a driving force, showcasing substantial inflows of $349.2 million during this recent week.

As J.P. Morgan’s strategists highlighted, the high-yield muni scene appears to be normalizing, with $20 billion in issuance recorded year-to-date, contrasting sharply with the relatively low figures seen in 2023. This restoration of balance comes as demand for yield continuously outstrips what the market can provide. Investors’ hunger for high-yield paper remains intense, now totaling $12 billion and $26 billion in inflows into high-yield and long-dated categories, respectively. The statistics reflect a market environment rich in opportunities, making munis a vital consideration for a variety of investors.

Interestingly, this year’s trend defies historical patterns. September could potentially break away from its normal behavior, where yields tend to rise. Olsan noted, “September is setting up to reverse the usual pattern for the month — when not since 2015 has the 10-year MMD spot finished lower in yield from August.” This shift illustrates a possible new era for municipal bonds driven by strong demand and emerging market dynamics.

Despite looming concerns about increased supply impacting yield, Olsan suggests that any potential yield rise may be reliant on significant external factors. The anticipation of outsized supply ahead of the election could lead to upward pressure on yields, yet these movements may be contained in the short term. High-tax bracket investors may discover appealing opportunities, particularly with intermediate AA-rated bonds trading at around 2.75%, equating to yield coverage of about 4.50%—positions that are enticing when compared to equivalent corporate bonds.

An example is identifiable in recent offerings, such as those by the Salt River Project Agricultural Improvement and Power District in Arizona, which showcased competitive 5s bonds for various terms that were well received. Demand continues to trend positively, as indications of larger issues utilizing 4% coupon structures beyond the 15-year mark emphasize robust support from both institutional and individual investors.

The current landscape of municipal bonds is dominated by unique market dynamics reflecting strong stability amidst varying influences. While anxieties surrounding supply growth exist, the underlying demand and continued inflow trends display the resilience and appeal of municipal bonds in today’s financial market environment. As we forge ahead, it will be vital for investors to stay attuned to these changes to harness potential opportunities effectively.