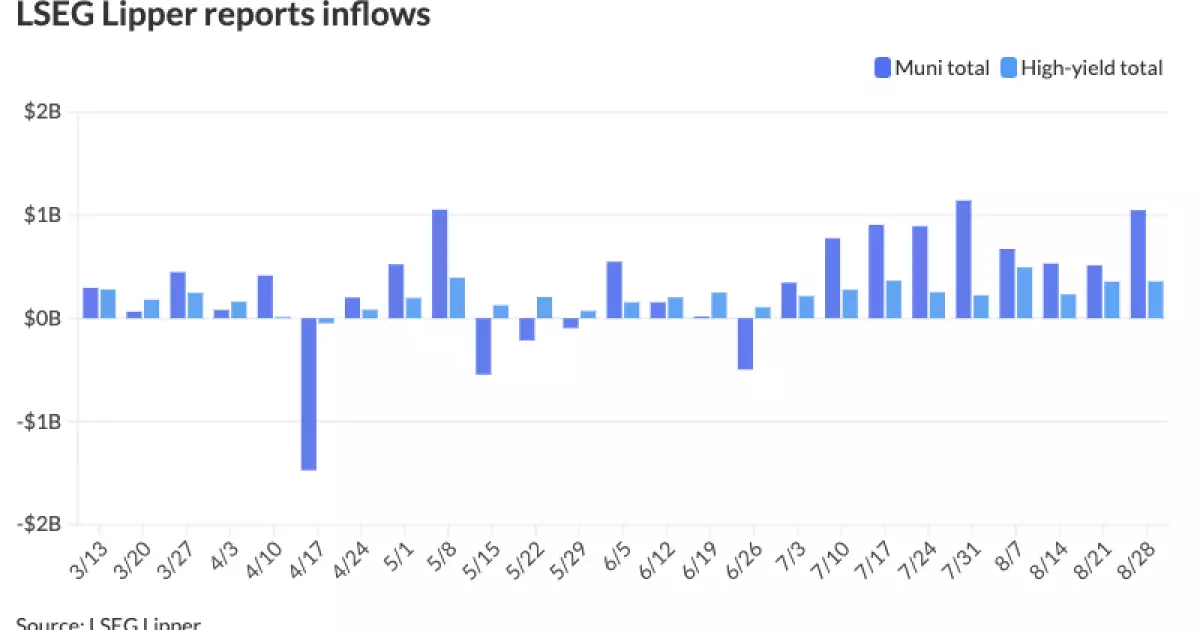

The municipal bond market has remained relatively stable, with municipal bonds seeing little change while U.S. Treasury yields have experienced an increase and equities have ended on a mixed note. Despite this stability, municipal bond mutual funds have seen inflows, with investors adding a significant amount of $1.047 billion to funds, following $512.9 million in inflows from the previous week. This consistent influx of funds marks nine straight weeks of inflows, indicating a certain level of confidence in the market.

High-yield bonds continue to show strength, with inflows of $357.5 million after the previous week’s $355 million. According to Kim Olsan, senior fixed income portfolio manager at NewSquare Capital, the market has been range-bound for multiple weeks, but the outlook for the fall suggests a more active period. Since August 12th, the 10-year U.S. Treasury range has been relatively narrow at 10 basis points, with the corresponding muni range even tighter. Issuers have taken advantage of this stability to come to the market in recent weeks.

One notable trend is the presence of the Billion-Dollar Club, where five unique issuers have priced $1 billion or more in bonds this month. This trend of billion-dollar-plus deals is becoming more common, with several months in 2024 seeing a similar number of sizable deals. For example, Chicago priced nearly $1 billion of Chicago O’Hare International Airport general airport senior lien revenue bonds, with slightly raised yields from preliminary pricing.

Despite record supply, the demand for municipal bonds remains high, with buyers focused on securing book income bought during a higher rate regime. The muni-UST valuations largely reflect the current risk landscape, with the two-year muni-to-Treasury ratio at 63%, the three-year at 65%, the five-year at 66%, the 10-year at 70%, and the 30-year at 87%. The market appears to be well-positioned for strategic opportunities, with strong inflows and eased secondary selling pressure.

As the year progresses, there may be a supply pause related to the upcoming election, setting the stage for a strong year-end. Tax policy will be a key focus in the coming year, with potential changes creating a positive tailwind for the market. Despite challenges such as federal debt, deficits, and lower growth odds, there is a sense of optimism regarding credit fundamentals, driven by record tax collections and prudent management practices.

Refinitiv MMD’s scale and other benchmarks have seen slight fluctuations, with some yields remaining unchanged while others have seen minor adjustments. The municipal bond market continues to attract investors seeking safe-haven flows, despite the peak in the rating cycle and ongoing economic uncertainties.

While the municipal bond market has shown signs of stability and strength, there are challenges and uncertainties on the horizon that could impact future trends. It is crucial for investors and market participants to closely monitor developments and adapt their strategies accordingly to navigate this ever-evolving landscape.