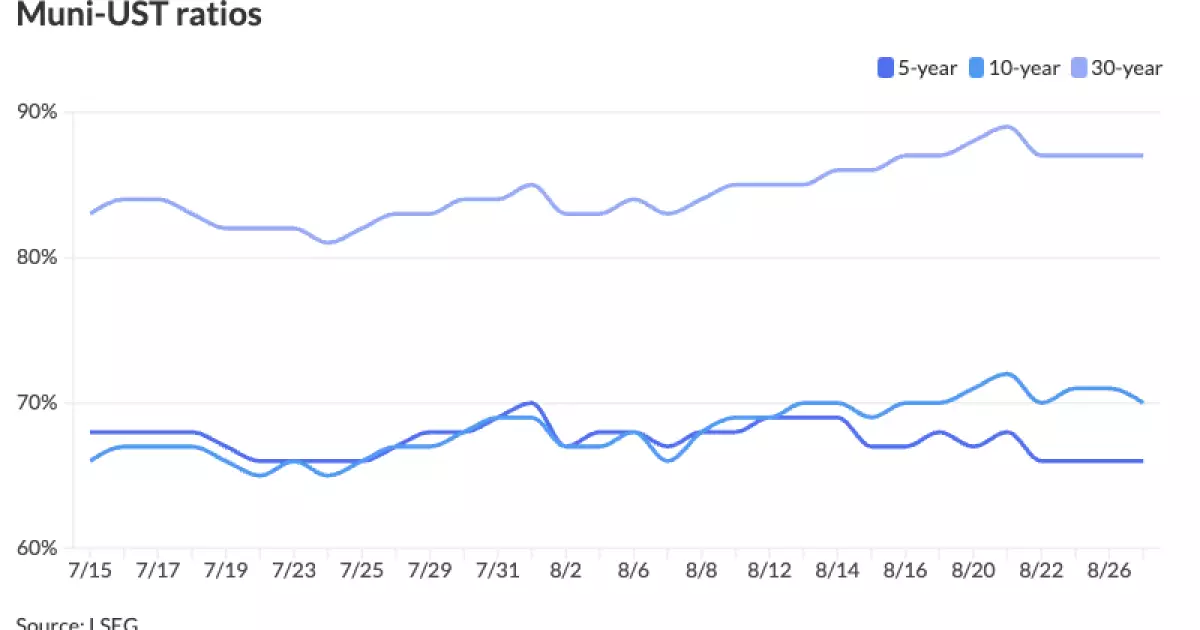

The municipal bond market saw mixed results on Tuesday as U.S. Treasury yields increased, while equities experienced a slight uptick towards the end of the trading day. This dynamic caused a variation in the muni-to-Treasury ratio across different maturities, with the two-year ratio at 63%, three-year at 66%, five-year at 66%, 10-year at 70%, and 30-year at 87% at 3 p.m. EST according to Refinitiv Municipal Market Data. ICE Data Services reported similar ratios at 3:30 p.m., with minor differences in percentages. Although the Federal Reserve’s decision to cut rates is expected to keep the Treasury market strong, leading to a positive outlook for municipals, some analysts still expect heavy issuance in the near term.

The primary market is currently offering attractive opportunities for investors to deploy capital, with significant supply expected in the coming weeks. Despite issuing nearly $9 billion in bonds this week, a substantial portion of which comes from two large deals, the appetite for municipal bonds remains robust. Various bond offerings were recently priced for institutions, with yields reflecting the prevailing market conditions and investor demand. For example, BofA Securities priced California’s various purpose General Obligation Bonds with yields cut inside 15 years and pushed out longer maturities for a substantial amount. Additionally, offerings from other entities like Maine Health and Higher Educational Facilities Authority, Pennsylvania State University, and Greenville, Texas, further illustrate the diverse opportunities available in the current market landscape.

Going forward, market experts predict continued heavy issuance in August, surpassing the figures from the previous year, with expectations of more significant deals in the pipeline. September is forecasted to see a sizable increase in both gross and net issuance, with demand for municipals remaining strong, particularly from institutional and sophisticated investors. Despite concerns about the impact of heightened issuance levels on market performance, many investors view this period as a buying opportunity given the temporary influx of bonds. Factors contributing to this trend include the approaching election season, prompting issuers to front-load their offerings to mitigate potential volatility post-election.

Key municipal bond scales, such as Refinitiv MMD, ICE AAA, S&P Global Market Intelligence, and Bloomberg BVAL, provide valuable insights into the yield curves for different maturity periods. These curves, although subject to fluctuations, offer a comprehensive view of the municipal bond market’s performance. Treasuries, on the other hand, experienced mixed results, further underscoring the volatility and interconnectedness between different segments of the fixed income market. Such fluctuations can impact investor sentiment and trading strategies, requiring market participants to remain vigilant and adapt to changing conditions.

Several notable offerings are set to enter the primary market, including bonds from entities like Chicago O’Hare International Airport, San Antonio, Texas, Utah Transit Authority, Texas Veterans Land Board, Indiana Finance Authority, University of Kentucky, and North Hempstead, New York. These diverse bond issuances represent the growing variety of investment opportunities accessible to market participants, each with its own unique characteristics and risk-return profiles. The competitive nature of the primary market adds another layer of complexity, compelling investors to conduct thorough due diligence and assess the suitability of each offering based on their investment objectives.

The municipal bond market continues to exhibit dynamic shifts driven by various economic and market factors. Investors must stay informed, exercise caution, and seek expert advice to navigate this complex landscape effectively. By analyzing current trends, anticipating future developments, and leveraging available resources, investors can capitalize on opportunities while managing risks in the ever-evolving municipal bond market.