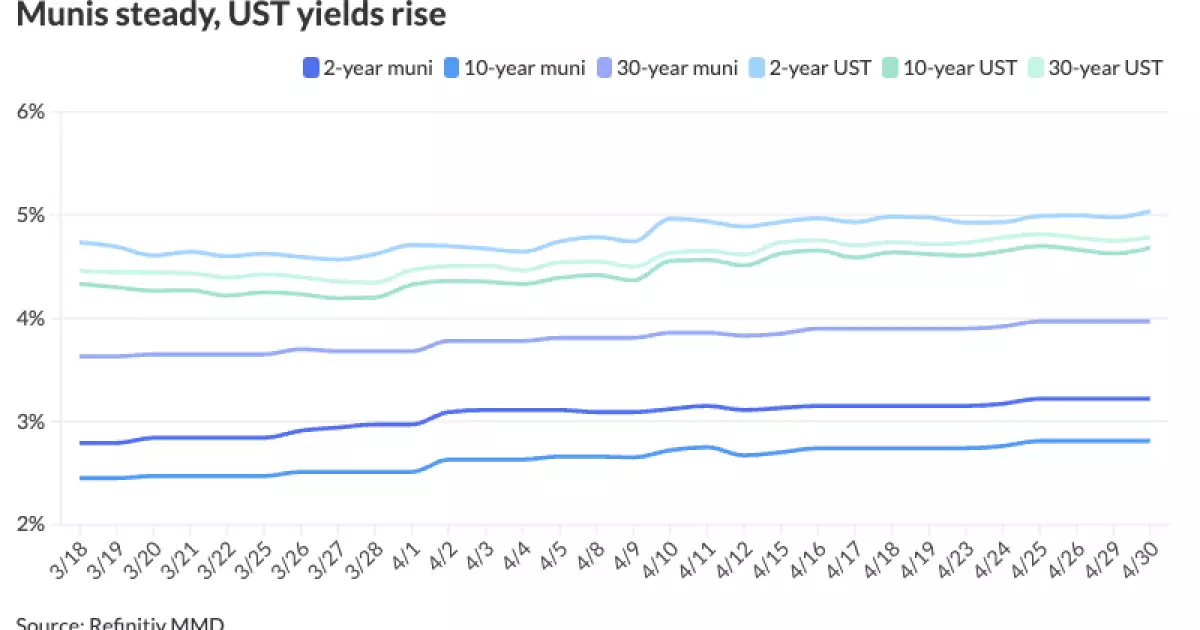

The municipal market has seen little movement in secondary trading, with the primary market taking center stage due to a number of deals being launched. Leading the pack is a substantial $1.9 billion Novant healthcare revenue bond deal in the negotiated market, alongside a general obligation sale from Delaware. While U.S. Treasuries experienced weakness, equities also took a hit. The yields on municipals were cut by up to two basis points, while UST yields climbed by as much as seven basis points, pushing the two-year UST above 5%, a level not seen since mid-November.

The recent increase in yields on municipals over the past few weeks has been attributed to a trend of larger supply in the tax-exempt sector. Matt Fabian, a partner at Municipal Market Analytics, pointed out that the 10-year MMD yield has risen by 35 basis points since March 1, with longer yields hovering around 4%. Despite this uptick in yields, there seems to be a growing comfort among retail buyers, as evidenced by the surge in customer net buying activity in recent days. The influx of issuance is providing opportunities, which investors are keen on seizing.

In the primary market, several notable deals have been priced and repriced by major players like J.P. Morgan, Siebert Williams Shank, Jefferies, and Raymond James. From Novant Health to the Port Authority of New York and New Jersey to the Texas A&M University System, a range of revenue bond and financing system bonds have been successfully issued. Institutions like the Illinois Housing Development Authority and the New Jersey Health Care Facilities Financing Authority have also made significant moves in the primary market.

Looking ahead, market experts like Anders S. Persson and Daniel J. Close from Nuveen anticipate the municipal market to stabilize as new-issuance subsides and investors gear up for the upcoming coupon reinvestment dates. They project substantial reinvestment income through the summer, with significant figures earmarked for May, June, and July. However, challenges remain, especially considering the recent underperformance of fund NAV returns, particularly in high yield strategies. The shifting landscape of muni holdings by banks also poses a potential hurdle for market stability.

The AAA scales across various data sources show minimal changes, with slight adjustments observed in different tenors. Refinitiv MMD, ICE AAA, S&P Global Market Intelligence, and Bloomberg BVAL have all reported similar trends in municipal yields. On the other hand, Treasuries experienced weakness, with increases seen across the board. The negotiated calendar highlights upcoming bond issuances, providing insights into the future trajectory of the municipal market.

The municipal market has witnessed substantial activity in the primary sector, with notable deals closing successfully. While market trends indicate a rise in yields, there is optimism regarding the stabilization of the market in the coming months. With strategic projections and ongoing market analyses, investors and institutions are gearing up for a period of potential opportunities and challenges. The municipal market continues to evolve, presenting a dynamic landscape for participants to navigate.