The municipal market experienced slight weakness in secondary trading on Wednesday, with a focus on the Los Angeles Unified School District’s nearly $3 billion pricing for institutions. This performance was influenced by the rise in U.S. Treasury yields and mixed results in equities. According to GW&K Investment Management strategists, munis entered the second quarter in “excellent shape,” with credit spreads falling within the fair value range and muni-UST ratios beginning to cheapen.

Additionally, J.P. Morgan strategists pointed out that the “muni AAA HG curve hit new year-to-date highs last week.” This has been accompanied by outperformance across the muni HG curve relative to the broader fixed-income market for the month. Despite this positive trend, absolute yields are still considered attractive in light of the trading range over the past three years and long-term projections for lower rates in the current year.

Ratios and Valuations

Refinitiv Municipal Market Data reported that the two-year muni-to-Treasury ratio on Wednesday was 64%, with other ratios falling in the 60-80% range for different tenors. ICE Data Services provided slightly different numbers, but the overall trend suggests that the two-year investment-grade muni ratios versus taxable fixed-income remain at transactional levels.

J.P. Morgan strategists emphasized that ratios tend to get richer towards the five to ten-year part of the curve. Despite this, the 10-year spot is still considered far more attractive in taxables versus tax-exempts. Furthermore, the longest portion of the tax-exempt market presents the most value, with 30-year AA tax-exempts falling within the middle of the trailing three-year range.

Despite expensive valuations, supply surges, and periods of low reinvestment demand, investor appetite for tax-exempts has remained steady throughout the quarter. GW&K Investment Management strategists pointed out the impressive stability in investor demand, which has withstood various market challenges. With the upcoming election campaigns intensifying, retail investors are being advised to secure muni yields due to potential increases in marginal tax rates.

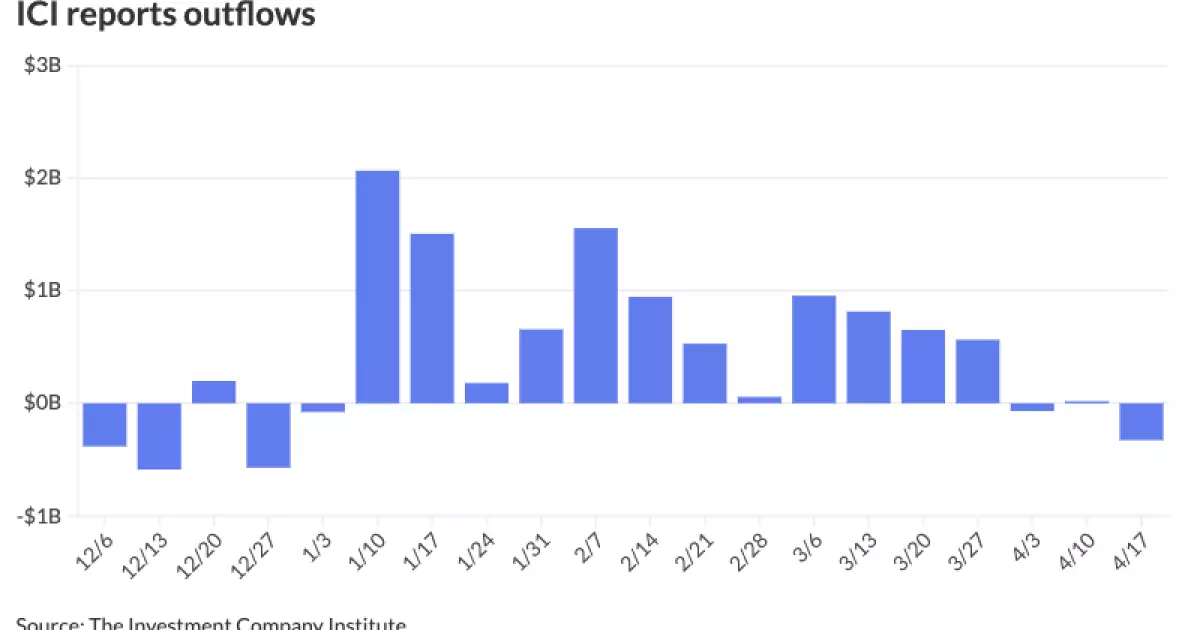

However, the Investment Company Institute reported outflows from municipal bond mutual funds for the week ending April 17. This marked a shift from the previous week’s inflows, indicating a cautious approach from investors. On the other hand, exchange-traded funds saw outflows following the previous week’s inflows as well.

In the primary market, several institutions priced new bond offerings. For instance, BofA Securities priced the Los Angeles Unified School District’s $2.984 billion of GO refunding bonds. Jefferies priced the New Jersey Health Care Facilities Financing Authority’s $370.735 million of RWJ Barnabas Health Obligated Group revenue and refunding bonds, while BofA Securities also priced the Maine Municipal Bond Bank’s $135.845 million of series A bonds.

In the competitive market, Denton County, Texas, sold $106.475 million of permanent improvement bonds to Jefferies. These pricing activities reflect the ongoing demand for municipal bonds from both institutional and retail investors.

Across different yield scales, there have been fluctuations in the municipal market. Refinitiv MMD, ICE AAA, S&P Global Market Intelligence, and Bloomberg BVAL all reported changes in their yield curves. The shifts in yields were observed in various tenors, indicating a dynamic market environment.

On the other hand, Treasuries were weaker on Wednesday, with yields showing an upward trend. This contrast between municipal and Treasury yields is reflective of the divergent movements in the fixed-income market, influenced by changing economic conditions and investor sentiment.

Looking ahead, several municipalities and entities are set to price new bond offerings. The Florida Development Finance Corp. plans to price $2.2 billion of Brightline Florida Passenger Rail Project tax-exempt AMT revenue refunding bonds. Valparaiso, Indiana, is slated to price $173.565 million of non-rated Pratt Paper, LLC Project exempt facilities refunding revenue bonds. Similarly, the Okaloosa Gas District, Florida, is expected to price $107.585 million of taxable and tax-exempt gas system revenue bonds.

These upcoming offerings highlight the continued activity in the municipal market and the diverse range of opportunities available to investors. It will be interesting to see how these new issuances are received by the market and the impact they have on the overall municipal bond landscape.