The municipal bond market was primarily focused on the primary market as investors assessed several large deals, while the secondary market took a backseat. U.S. Treasuries showed improvement and equities rallied based on earnings reports. This dynamic created a scenario where new issuances were on the rise, leading to elevated muni yields, as noted by experts such as Chris Brigati and Anders S. Persson. The demand for paper in the market was attributed to institutional municipal money managers needing large block sizes to align portfolios with their original mandates. Despite muni-UST ratios leaning towards the rich side, experts like Daniel J. Close highlighted the emergence of a new normal in market dynamics.

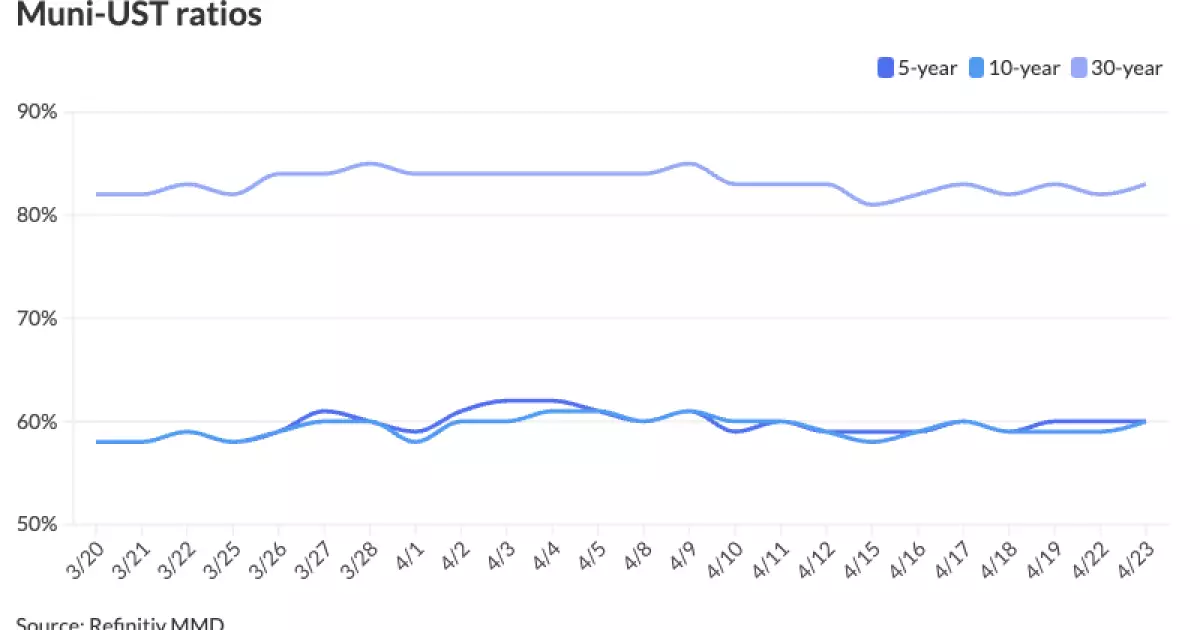

The muni-to-Treasury ratios for various maturity tenors reflected the market sentiment with the two-year at 64%, three-year at 63%, five-year at 60%, 10-year at 61%, and 30-year at 82%. This implied a preference for investments with longer tenors, possibly due to a fluctuating market landscape. A notable observation was the resilience of front-end yields compared to widening term spreads, indicating diversified investor demand. Specifically, the bid strength from separately managed accounts and retail investors contributed to this market behavior. Matt Fabian highlighted this trend and emphasized the importance of considering different investor profiles in the current market scenario.

On the flip side, the back end of the curve, typically supported by institutions, faced challenges in terms of demand and reinvestment prospects. With May approaching, which historically marks a challenging reinvestment period, near-term optimism was hard to find. However, well-structured credits in the primary market continued to see strong demand, presenting opportunities for income-focused investors. The emergence of tax-exempt products, potentially through Build America Bond refundings, further enriched the market landscape for discerning investors. This created a scenario where income-focused buyers could capitalize on structured products outside typical retail ranges for optimal returns.

A detailed analysis of primary market activities showcased significant deals such as the Los Angeles Unified School District’s GO refunding bonds and Houston’s combined utility system revenue refunding bonds. Noteworthy transactions included Energy Northwest’s revenue and refunding bonds and Oregon’s general obligations, indicating a mix of sectors and issuers in the market. The pricing and demand for these deals reflected market dynamics, with a focus on yield, callability, and maturity profiles. This critical evaluation of primary market activities provided insights into investor behavior and confidence in different credit instruments.

Various market benchmarks, including Refinitiv MMD, ICE, S&P Global Market Intelligence, and Bloomberg BVAL, provided insights into yield curve movements and comparative analysis. These benchmarks reflected changes in yields across different tenors, illustrating the evolving market conditions and investor sentiments. The stability of AAA scales indicated a cautious approach by investors, considering the broader economic landscape and policy frameworks. Furthermore, the performance of U.S. Treasuries played a crucial role in shaping investor decisions, with slight improvements noted in short to long-term Treasury yields.

The negotiated calendar highlighted upcoming offerings from various issuers, including Brightline Trains Florida, RWJ Barnabas Health, and Christus Health. These offerings provided a glimpse into the diverse range of projects and sectors seeking financing in the municipal bond market. The competitive market also featured offerings from Denton County, Valparaiso, and Frisco Independent School District, showcasing a mix of rated and non-rated bonds. This diverse landscape presents opportunities for investors to diversify their portfolios and capitalize on different risk-return profiles. Overall, the market outlook appeared optimistic, albeit with challenges related to reinvestment and yield expectations.

The municipal bond market continues to evolve, presenting a dynamic landscape for investors to navigate. Understanding market trends, investor behavior, and upcoming offerings is crucial for making informed investment decisions. While challenges such as reinvestment uncertainties and yield fluctuations persist, opportunities in well-structured credits and diverse offerings provide avenues for income-focused buyers to optimize their returns. By critically analyzing market movements, investors can better position themselves to navigate the complexities of the municipal bond market and capture potential opportunities for growth and stability.