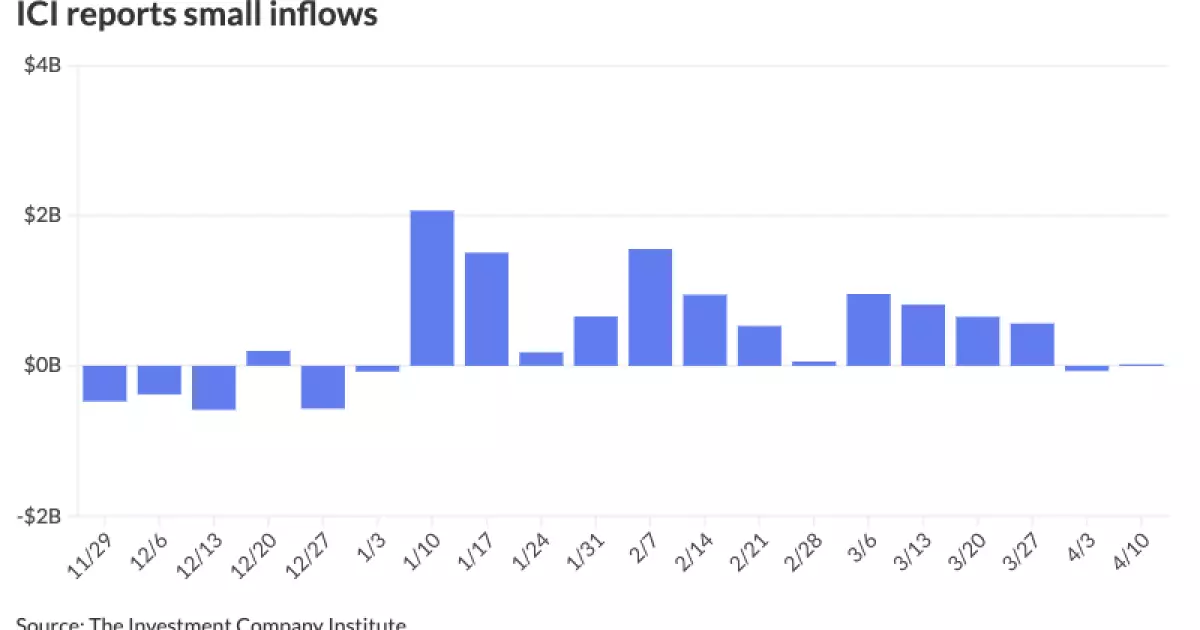

The municipal bond market experienced little change on Wednesday due to a slowdown in supply and small inflows into muni mutual funds. Despite this, U.S. Treasury yields declined, and equities faced losses, showcasing a complex interplay of factors affecting the market. The Investment Company Institute reported modest inflows into municipal bond mutual funds for the week ending April 10, with $18 million being added following $69 million of outflows the previous week. On the other hand, exchange-traded funds witnessed significant inflows of $944 million after $19 million of outflows in the preceding week.

According to J.P. Morgan strategists, the yield across all spots on the muni AAA HG curve reached new year-to-date highs, with the municipal high-grade curve demonstrating outperformance relative to the broader fixed-income market this month. Jeff Timlin, a managing partner at Sage Advisory, acknowledged the “rapid” U.S. Treasury volatility, which has presented challenges in predicting muni yield movements. However, he noted that the volatility has not deterred the new-issue market’s strength, attributing it to the abundance of capital available for investment.

J.P. Morgan strategists highlighted that despite last week’s richening, the two-year investment-grade muni ratios in comparison to taxable fixed-income are at “transactional levels.” They emphasized that ratios become progressively richer in the five- to 10-year part of the curve, with the 10-year spot still favoring taxables over tax-exempts. Refinitiv Municipal Market Data and ICE Data Services provided insights into the muni-to-Treasury ratio, showcasing variations across different maturity points on the curve. The strategists identified the longest part of the curve in the tax-exempt market as having the most apparent value given the prevailing ratios.

J.P. Morgan strategists offered a cautious outlook, mentioning that current valuations and technical expectations suggest potential underperformance in a less favorable environment in April. They forecast April as a relatively softer period due to the expected supply influx until early June, creating opportunities for investors to reallocate capital. Timlin echoed these sentiments, noting that reinvestment dollars are expected to increase from June through August, marking a crucial phase for maturity and coupon payments in the market.

The Bond Buyer 30-day visible supply stood at $8.93 billion, indicating the volume of potential bonds entering the market. Various yield curves from Refinitiv MMD, ICE, S&P Global Market Intelligence, and Bloomberg BVAL exhibited minor changes in yields across different maturity points, reflecting the market’s stability and slight fluctuations. Treasuries saw firmness across the curve, indicating investor confidence in government-backed securities.

Several entities, including the Arizona Board of Regents, Washington State Housing Finance Commission, Oklahoma Capital Improvement Authority, Oregon Department of Administrative Services, and Wake County, North Carolina, are set to price bonds on Thursday, presenting opportunities for investors to participate in diverse offerings. Additionally, competitive sales from Albuquerque, New Mexico, and Clark County School District, Nevada, signify active participation in the municipal bond market.

The municipal bond market continues to navigate through a dynamic environment characterized by supply-demand dynamics, yield fluctuations, and investor sentiments. Despite challenges posed by market volatility and supply influx, opportunities exist for investors to strategically position themselves in the market based on expert insights and upcoming bond offerings. Vigilance and a deep understanding of the market trends are essential for maximizing returns and managing risks in the municipal bond market landscape.