As of mid-February 2024, the municipal bond market has experienced a state of relative stability amidst fluctuating conditions in other financial sectors. On Wednesday, municipal bonds exhibited minor changes as U.S. Treasury yields firmed up, with equities showing mixed results. Key metrics showcasing the health of municipal bonds highlighted a consistent ratio of two-year bonds compared to U.S. Treasuries (UST), maintaining a steady 63%. The ratios for five-year and ten-year bonds also reflected a similar trend, while thirty-year bonds reported an 84% ratio.

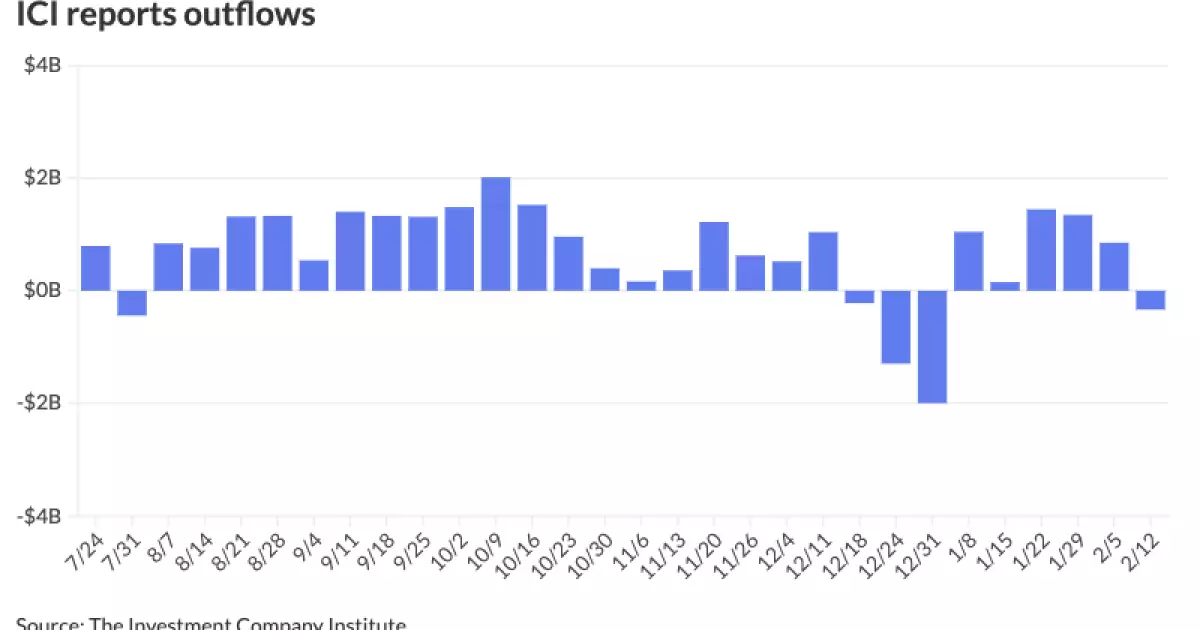

In this context, the Investment Company Institute (ICI) reported significant outflows of $336 million in the week ending February 12. This shift followed a previous week of inflows totaling $852 million. Contrastingly, LSEG Lipper indicated $238.5 million in inflows, pointing to diverging perspectives on market liquidity. Furthermore, the exchange-traded funds (ETFs) sector saw a substantial uptick of $1.385 billion in inflows, emphasizing a notable interest in municipal investments despite overall outflows.

The municipal bond market is entering a phase where supply is anticipated to exceed $500 billion in 2024. This surge is attributed largely to a swell in demand for funding long-delayed infrastructure projects, driven in part by the exhaustion of COVID-era financial assistance. Nick Venditti, a leader in municipal fixed income at Allspring, articulated that issuers can no longer afford to delay bond issuance as they did in the past two years. The urgency to access capital markets exposes the pressing infrastructure needs of many regions and municipalities.

Last week served as a prime example of this increased issuance, marked as the fifth largest in the last year. However, experts suggest that while the demand from institutional investors remains robust, other market participants, particularly those utilizing separately managed accounts, may exhibit hesitation if nominal prices dip significantly. This introduces an element of caution, embedding a potential vulnerability in market stability.

While issuance is projected to decline to approximately $5.5 billion this week—partly due to the Monday holiday—it is expected to ramp up in the following weeks. The core question moving forward lies in whether the enthusiastic demand seen earlier in the year can maintain its momentum amid an influx of new supply. Venditti cautioned that an imbalance—should supply outpace demand—could weigh heavily on the municipal market, potentially hindering its recovery trajectory.

In the primary market, notable issuances are on the horizon. BofA Securities is preparing to launch a considerable offering for the Pennsylvania Economic Development Financing Authority. The offering consists of $500 million in taxable bonds intended to finance essential economic development and infrastructure initiatives with varying maturities, calling for bonds issued as far out as 2054. This established issuer’s backing and the diverse range of maturities underscore the ongoing demand for funding long-range projects.

Additionally, other municipalities are also gearing up for significant bond offerings, including the Miami-Dade County’s airport revenue bonds and revenue financing bonds for the Texas Tech University System. These upcoming issuances indicate a noteworthy intent among various issuers to capture what could be a beneficial market environment for raising funds.

A comprehensive analysis of yield curves reveals little change in municipal bond yields, with one-year and two-year AAA rates remaining constant at 2.66% and 2.68%, respectively. Meanwhile, five-year and ten-year yields are consistently at 2.76% and 3.00%. These figures represent a calm before what many are speculating could be a significant shift in variables influencing market performance.

Treasuries also showcased stability, with the two-year UST yielding 4.271%. These numbers result in a relatively predictable environment, crucial for investors eyeing the municipal bonds for risk-adjusted returns. Analysts are keenly observing whether the yield environment will stimulate new investment flows or if existing investors will capitalize on the persistent demand for quality bonds.

To summarize, while the municipal bond market faces pressures from changing supply dynamics and transactional hesitancy, it remains buoyed by robust institutional demand amid rising issuance. As municipalities pursue essential funding for infrastructure improvements, the question becomes whether demand can sustain pace with supply. Investors should remain vigilant, prepared for shifts that could redefine market trajectories in the coming weeks, emphasizing the need for agility amidst evolving economic landscapes.