As December draws to a close, the municipal bond market finds itself grappling with notable challenges, primarily induced by persistent volatility in U.S. Treasury yields. The absence of substantial new issues has further complicated the landscape, leaving municipal bonds to navigate through a tumultuous period marked by losses in equities and Treasuries alike. As the year comes to an end, analyses suggest that municipal bonds will finish in negative territory, mirroring broader market trends affected by macroeconomic uncertainties.

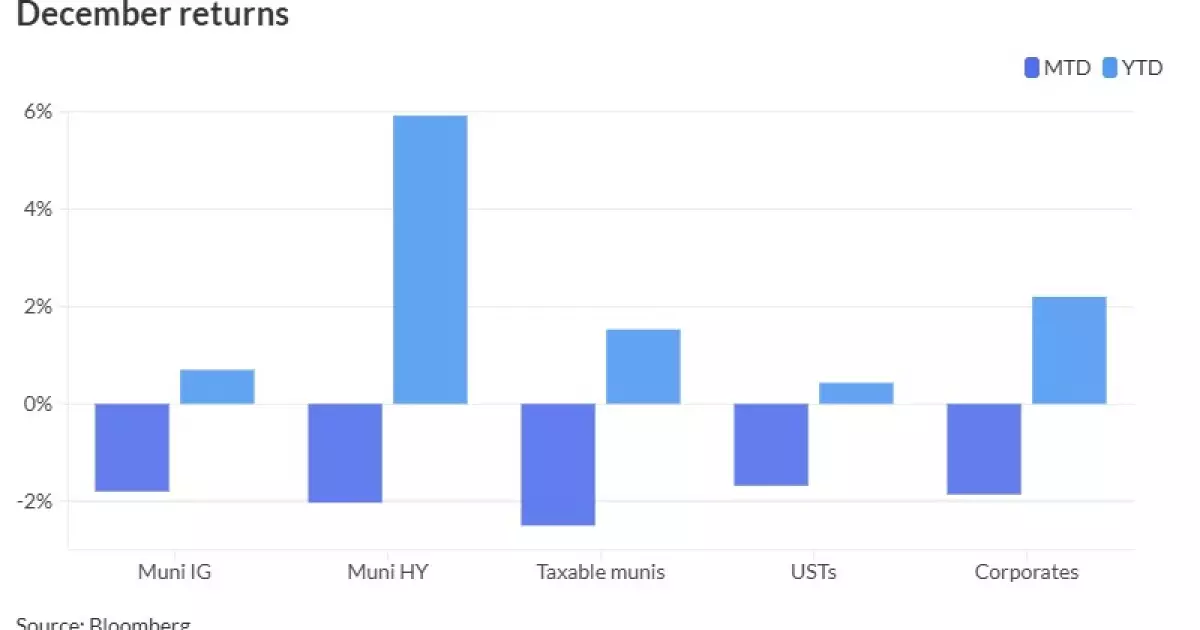

The Bloomberg Municipal Index is indicative of this downturn, registering a decline of 1.80% for December, despite a modest gain of 0.70% year-to-date. High-yield municipal bonds are not faring much better, experiencing a loss of 2.03% this month, although they boast a commendable return of 5.92% for the year, underscoring the inherent volatility that defines municipal bonds as we approach the new year. Meanwhile, taxable municipal bonds show a similar pattern, losing 2.50% in December while remaining up by 1.53% year-to-date.

This duality of performance reflects broader trends in the UST market, which reported losses of 1.68% for December, predominantly characterized by a concerning yield increase—culminating in the 10-year UST closing above 4.6%. Such movements in Treasury yields could exert upward pressure on municipal yields, further complicating the decision-making process for municipal bond investors.

Looking ahead, the balance of supply and demand in the municipal market will significantly influence trading dynamics. A notable observation comes from Kim Olsan, a senior fixed-income portfolio manager. According to Olsan, with the 30-day visible municipal supply currently at $5.55 billion, an $8 billion gap exists between expected supply and implied demand from redemptions. This discrepancy is crucial, as it suggests a tightening in the market capable of producing upward pressure on yields should appetite for individual components wane, especially before crucial Federal Open Market Committee (FOMC) discussions.

Additionally, January appears set to bring a greater influx of new issues, particularly from reliable sources such as Washington State, which plans to introduce over a billion dollars in general obligation bonds. Despite concerns over Treasury volatility, January has historically provided favorable conditions for municipal bonds, making it imperative for investors to stay attuned to upcoming supply dynamics.

Investors are right to be cautious, given the potential for market shocks due to coordinated fiscal changes or changes resulting from tax reforms. Matthew Norton, chief investment officer for municipal bonds, notes that an influx of high supply, coupled with Treasury rate volatility, could lead to significant anxiety among investors, potentially resulting in net outflows from mutual funds focused on municipal bonds.

Despite some challenges this December, the overall fund flow has been relatively positive compared to previous years, highlighting a stabilizing tendency amidst fluctuations. The lack of a “negative loop” seen in past years—where upwardly trending yields trigger NAV losses and subsequent outflows—has allowed some confidence to persist.

Evaluating Credit Quality’s Performance

One noteworthy trend this year has been the relative outperformance of lower-rated municipal credits, contrasting sharply with previous patterns favoring higher-rated bonds. Olsan’s analysis of spreads between A-rated and AAA-rated instruments reveals an encouraging story—spreads have remained remarkably stable, reflecting a degree of investor confidence that has not vanished despite turbulent market conditions.

Returns in the single-A category have consistently outstripped higher-rated offerings, with Bloomberg Barclays’ A-rated index gaining 1.4%, outperforming the broader municipal index by a significant margin. This trend indicates that while investors remain wary of broader market volatility, there is an underlying recognition of value in select lower-rated bonds.

As we transition into the new year, the municipal bond market is poised at a precipice of uncertainty. With an evolving macroeconomic environment, including potential tax reforms and policy adjustments expected from the FOMC, municipal investors must remain vigilant. While anticipations for January are promising, the interplay between supply constraints and Treasury volatility presents a delicate balance that may determine future performance.

Investors will need to adapt quickly to ensure that they are taking advantage of potential opportunities while being prepared for shifts in the broader market dynamics. The coming weeks will undoubtedly be critical in shaping the trajectory of the municipal bond landscape as we venture into 2024.