The municipal bond market has undergone noteworthy transformations in the third quarter of 2024, driven by a complex interplay of supply dynamics and shifts in investor patterns. Fed data highlights significant participation from mutual funds, exchange-traded funds (ETFs), and foreign buyers, indicating a rising interest in municipal assets. This article will delve into the current state of the municipal bond market, examining ownership trends, regulatory challenges, and the broader implications for financial institutions and investors.

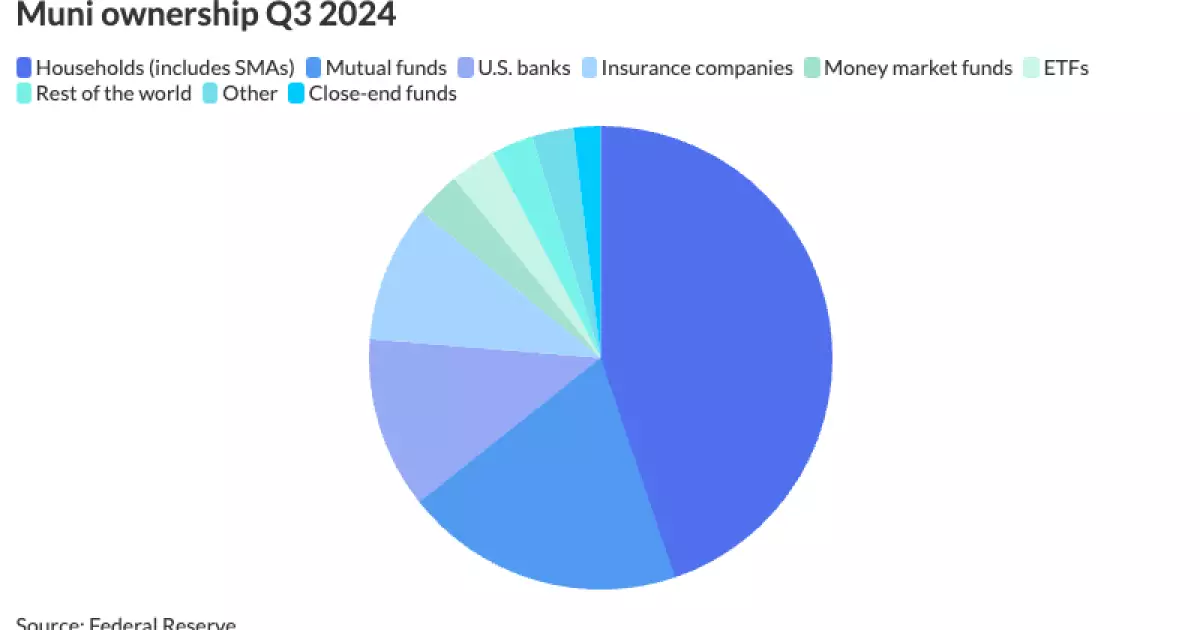

Despite an overall increase in the municipal bond market, it is crucial to note that the ownership levels held by institutional investors, particularly banks, have faced considerable declines. According to Barclays, bank holdings of munis have reduced to $497.2 billion, marking a 0.3% decrease from the previous quarter and a substantial 4.3% drop compared to Q3 of 2023. This trend raises concerns about the reliability of banks as steady players in the municipal bond space, particularly smaller and medium-sized banks that have been grappling with deposit outflows and regulatory constraints over the past few years.

The conundrum emerges primarily from the shrinking balance sheets of regional banks, which, in turn, diminishes their appetite for high-grade municipal bonds. The Wells Fargo strategists attribute this decline in bank ownership to a reduced deposit base. Such a scenario leaves these institutions with less capital to invest, thus highlighting a major risk factor for the broader economy. Conversely, larger banks seem to maintain a cautious approach despite the potential for deposit base growth.

Looking into the future, the outlook changes as Wells Fargo suggests that deregulation could offer some relief to banks grappling with capital constraints. As regulatory barriers diminish, the market could see an increase in demand for high-quality municipal debt, potentially revitalizing interest from banks and institutional investors. The balance shifts in the ownership of municipal debt are crucial to monitoring the sector’s health in the coming years.

Interestingly, the face amount of munis outstanding rose to $4.171 trillion, representing a 0.8% increase from Q2 2024 and a more substantial 2.9% compared to a year prior. This statistical growth serves to illustrate the environment’s dichotomy—growing supply amidst declining institutional ownership reveals a market caught between demand dynamics and restrictive lending practices.

Household and Foreign Investment Trends

An increasingly diversified ownership structure is evident as households emerged as the largest category of municipal bond owners, possessing 44.8% of total holdings. The surge in household ownership reached $1.86 trillion, driven primarily by the growth of separately managed accounts (SMAs), which alone account for a staggering $1.63 trillion. These accounts allow individuals to invest directly in municipal securities with significant control over their portfolios, reflecting a shift towards personalized investment strategies.

Additionally, the role of foreign investors in the U.S. municipal bond market proved pertinent, with foreign ownership climbing to $121.5 billion, a notable increase of 2.6% from the previous quarter. Diversifying portfolios with municipal bonds appears to be an attractive strategy for foreign investors, possibly due to their relative stability amidst global market uncertainties.

A defining characteristic of this market wave has been the contrasting performance of mutual funds and ETFs. In Q3 2024, mutual funds in the municipal segment witnessed an increase to $810.9 billion, marking a 4% growth from Q2. Meanwhile, ETFs experienced a remarkable surge, rising to $133.3 billion—up 7.2% in comparison. This growing inclination towards ETFs underscores a gradual shift from actively managed funds towards passive investment vehicles, identified as more cost-effective due to their lower transaction costs.

Strategists at Wells Fargo note that the active-to-passive transition signifies investors’ growing comfort with index-based strategies, especially in a low-stress credit environment. This trend has far-reaching implications, as passive strategies provide competitive returns that align well with investor goals while minimizing costs.

The municipal bond market’s landscape in Q3 2024 suggests an evolving ecosystem shaped by various interests and financial forces. As institutional ownership declines amid regulations and deposit challenges, the increasing strength of household and foreign investors provides a counterbalance. The mutual fund and ETF performance highlights a transition in investor strategy, creating a potential shift in future asset allocation practices.

The interactions and adjustments observed in the municipal bond market are indicative of broader economic trends. The trajectory ahead is contingent on how well financial institutions adapt to these dynamics, the implications of deregulation, and the evolving preferences of investors navigating an ever-changing fiscal landscape. As we look towards the future, staying informed and adaptable remains paramount for all market participants.