The municipal bond market has entered a dynamic phase characterized by notable fluctuations in trading activity, with investors and analysts keenly observing various economic indicators. This article will explore the recent trends in municipal bonds, mutual fund inflows, and the implications for future market behavior, drawing insights from recent data and expert opinions.

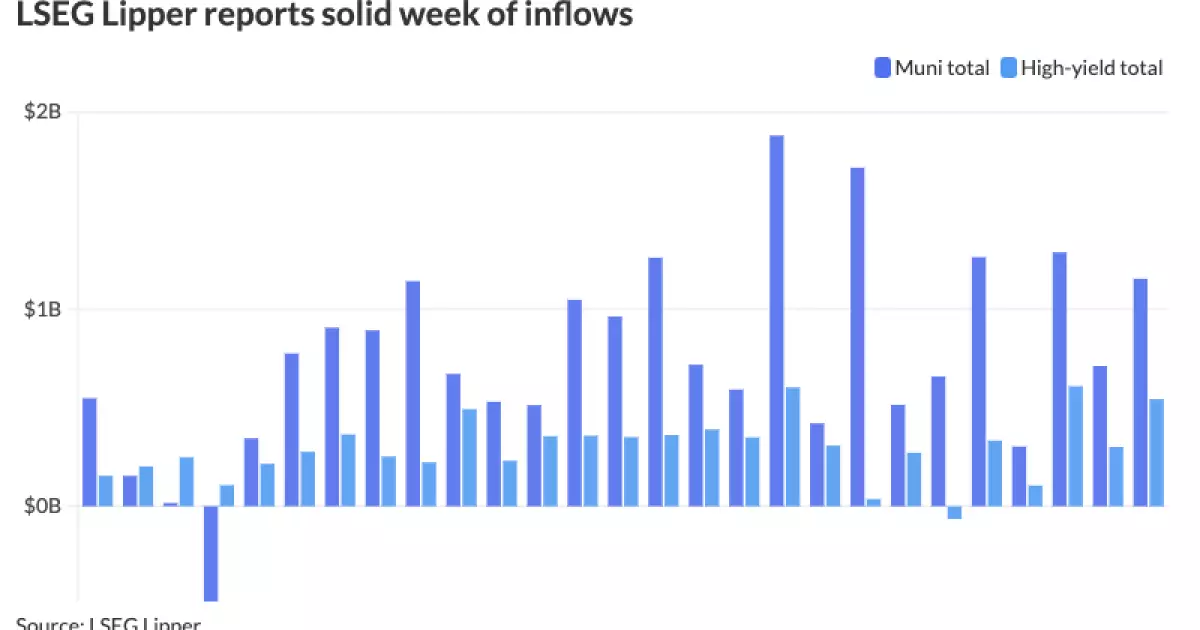

Recent reports from Lipper indicate encouraging trends for municipal bonds, particularly in mutual fund inflows, which exceeded $1 billion for the week ending December 4. This figure marks a significant increase from the previous week’s revised total of approximately $711.5 million. Notably, high-yield municipal bond funds attracted $534.1 million, a rise from $300.6 million the week prior. These inflows suggest a robust interest among investors in the municipal bond sector, contradicting any lingering fatigue that might have set in from previous market volatility.

Chris Brigati, a senior vice president at SWBC, has emphasized this phenomenon, indicating that investor appetite for municipal securities remains strong. He notes that the consistent inflow of funds reflects a persistent belief in the market’s potential, highlighting that investors continue to seek opportunities amidst broader economic concerns.

In analyzing the municipal bond market, one key metric is the ratio of municipal bonds to U.S. Treasuries (UST). Recent readings from Refinitiv Municipal Market Data reveal that the two-year municipal to UST ratio stands at 61%, while other maturities are as follows: five-year at 63%, 10-year at 65%, and 30-year at 82%. These ratios suggest that municipal bonds are relatively attractive compared to Treasuries, especially in the longer-term maturities, aligning with Brigati’s optimism regarding continued strong demand in the upcoming months.

However, the primary market is preparing for significant activity as the end of the year approaches. Traditionally, December has been a strong month for municipal bond issuance, with average volumes around $31 billion since 2013. Given current market conditions, experts like Matt Fabian from Municipal Market Analytics anticipate that the forthcoming volume could reach approximately $500 billion, contingent on issuer perceptions of risk and the impact of potential tax legislation changes on the municipal bond landscape.

The ongoing dialogue surrounding the tax exemption for municipal bonds is gaining traction, as both major political parties recognize the necessity for infrastructure improvements. Analysts, including Matthew Norton and Daryl Clements from AllianceBernstein, express that losing this tax exemption would not only strain economic growth but also hinder critical infrastructure investment across the United States.

Interestingly, the potential economic implications of removing or limiting the tax exemption are substantial given that it would save the federal government merely $40 billion annually—a fraction of the $6.5 trillion federal budget. Both Norton and Clements emphasize that preserving the exemption is essential, as stripping it would throw infrastructure financing into chaos, undermining local economies and community development initiatives.

On the primary market front, several large transactions have occurred recently, reflecting the heightened interest in municipal bonds. Notably, Barclays priced $1.5 billion of transportation program bonds for the New Jersey Transportation Trust Fund Authority, with maturities ranging from 2024 to 2055 and yields varying from 2.90% to 4.21%. Additionally, J.P. Morgan Securities managed the pricing of $772.65 million in airport facilities revenue bonds for the Greater Orlando Aviation Authority, showcasing robust investor interests in essential infrastructure projects.

Further diversifying the market, RBC Capital Markets and BofA Securities have also introduced substantial issuances, reflecting a blend of senior and subordinate bonds that cater to varying risk appetites. Each transaction not only signals investor confidence but also indicates the continuous need for financing avenues for state and local governments aiming to address pressing fiscal demands.

The municipal bond market appears well-poised for continued investor interest as we move into 2024. The influx of mutual funds, supportive economic ratios, and ongoing discussions regarding tax exemptions should underpin market stability. However, vigilance is essential, as market participants must remain attentive to policy changes and broader economic conditions that may influence municipal bond performance in the upcoming months. Ultimately, the interplay between infrastructure demands and investor appetite will shape the trajectory of this vital segment of the financial landscape.