The municipal bond market is reflecting a fascinating dynamic of yield adjustments, evolving investor sentiment, and strategic issuance that is a lot to unpack. The interplay between municipal bond performance and U.S. Treasury yields reveals critical insights into market behavior, demand, and future outlook.

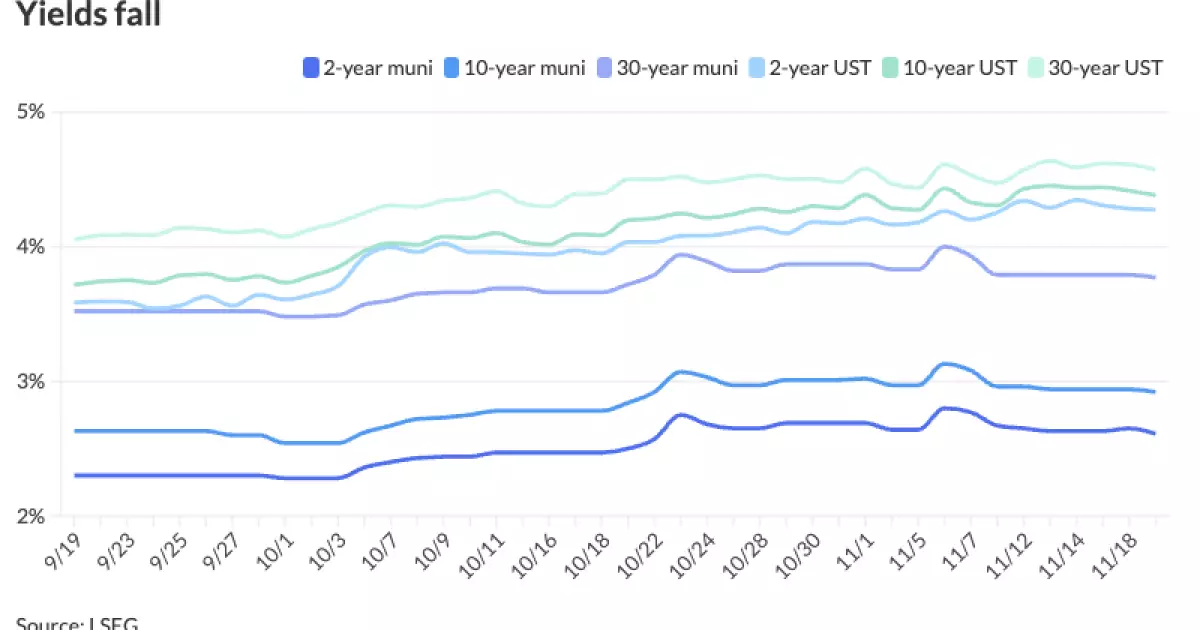

Recent trends show a notable dip in U.S. Treasury yields, which had a cascading positive effect on municipal bonds. The yields on triple-A rated municipal bonds experienced an increase ranging from one to six basis points, a reflection of the overall market sentiment as equities displayed mixed performance. These variations underscore the intricate relationship between munis and Treasuries, where market participants often adjust their strategies based on broader economic indicators.

This week’s market performance, particularly on Tuesday, spotlighted an interesting scenario where the primary market took precedence over the secondary market. The infusion of several large new issues—such as the extraordinary $1 billion high-yield United Airlines Terminal project—underscored the continuing investor appetite for riskier yet potentially lucrative investments. This heightened demand is illustrated by comments from industry experts like Chris Brigati, who emphasized that despite a generally lighter issuance calendar, the week’s supply remained robust enough to entice investors.

Chris Brigati pointed out that the pent-up demand amongst investors serves as a buffer, effectively absorbing the new debt offerings while keeping ratios tight. This phenomenon is critical as it suggests that even with a lighter calendar, the municipal bond market remains resilient, drawing in significant investment interest. The ratios reported by Municipal Market Analytics demonstrate how competitive the market has become, especially for shorter maturities. For instance, the two-year municipal to UST ratio at 61% exhibits a trend towards increasingly attractive pricing.

However, as Matt Fabian pointed out, while the yields themselves remain compelling, the imminent question is whether this momentum can be sustained as we approach year-end. With historical data indicating that just four of the past fifteen years experienced similar positive inflows, expectations for the upcoming months hinge on both market performance and supply dynamics.

The influx of total trade counts exceeding 300,000 last week reinstates confidence in retail demand. A significant shift in investor strategies is noted, with many retail investors gravitating towards separately managed accounts, a departure from traditional mutual and exchange-traded funds. This shift may be attributable to a growing search for better income channels, especially given the current economic climate marked by inflation concerns and market volatility.

The modest inflows into mutual funds and ETFs reveal a complex picture. While mutual funds have seen healthy inflows expected to reach $30 billion for the year (excluding ETFs), market analysts are cautious regarding the sustainability of this growth. Fabian’s remarks regarding the necessity for yields to align with market demand hint at future volatility that might provide both challenges and opportunities for savvy investors.

Looking ahead, the question of how much more supply will emerge before year-end is pivotal. Last year’s supply figures exceeding $45 billion set a benchmark that current market conditions must meet or exceed to maintain equilibrium. With over $451 billion already logged this year, the potential for nearing the $500 billion mark raises concerns regarding the balance of supply and investor demand.

To achieve this milestone, analysts believe a radical shift in yields may be necessary—whereby incremental price declines could stimulate further interest. The historical performance of UST bonds, particularly under rising inflation and credit fears, will significantly influence municipal bond market trajectories.

The primary market has showcased several attractive offerings this week. Noteworthy issuances included BofA Securities pricing $1.1 billion in revenue bonds for airport system upgrades in Houston and Goldman Sachs facilitating a $782 million green energy bonds deal for California. Additionally, the variety of projects—from transportation infrastructure to housing finance programs—illustrates the breadth and diversity within the municipal bond sphere.

Investors’ response to these offerings is critical. The robust pricing strategy employed by financial institutions, along with the calculated issuance of securities, aims to mitigate risk while appealing to a diverse array of investors. The magnitude of demand for various bond issues, particularly at competitive rates, sets the stage for an interesting conclusion to 2023.

The current municipal bond landscape resonates with optimism amidst challenges. Understanding the synergy between U.S. Treasuries and the broader economic context will be crucial as market participants navigate these evolving trends. As we enter the final months of the year, vigilance in tracking supply timelines and investor behavior will be essential for fostering an informed investment strategy.