The municipal bond market has witnessed a period of stability and consistent performance leading into the Thanksgiving holiday week. With light trading that resulted in only minor fluctuations in yields, the market reflects a clear trend of municipal outperformance compared to U.S. Treasuries and corporate bonds. This analysis delves into the latest developments in the municipal market, examining both the underlying technical factors and the outlook for the coming months.

The recent trading session showed that triple-A municipal yield levels have remained virtually unchanged for nine consecutive days. This stability comes in the context of a broader environment where U.S. Treasury yields experienced slight changes—specifically some losses at the short end of the curve while longer-term rates showed modest gains. Peter DeGroot of J.P. Morgan notes that the technical strengths in the municipal market have facilitated significant outperformance this November.

Several factors have contributed to this landscape. One primary driver has been the notable decrease in supply. As fewer new bonds hit the market, dealers have seen their inventories decline considerably. In addition, there seems to be little apprehension from retail investors regarding potential volatility in interest rates or tax-exempt bond threats, as evidenced by the continued investment flow into municipal bonds. Mikhail Foux from Barclays highlights that the tax-exempt ratios now maintain a more balanced stance compared to corporate bonds across various maturity ranges.

The performance metrics reveal a remarkable advantage for high-grade municipals. In November alone, these securities have outperformed Treasuries significantly across various maturities, with the two-year, five-year, ten-year, and thirty-year bonds yielding higher by 26, 17, 24, and 25 basis points, respectively. The current ratios indicate a tight market: the two-year municipal to UST ratio stands at 60%, creeping up to 82% for the 30-year bond.

However, Foux expresses caution regarding potential investor exuberance in chasing performance due to less appealing ratios. Consequently, the trading activity has seen a marked decrease as market participants remain focused on upcoming new issues, perhaps suggesting a more defensive posture among investors.

As we approach the Thanksgiving holiday week, investors can expect approximately $1.4 billion in new issuances, with the market’s visible supply sitting at around $6.91 billion. The anticipated decline in net supply moving into December—from $17 billion this month to $3 billion—suggests a supportive technical backdrop for continued municipal outperformance. Yet, DeGroot appropriately cautions that replicating November’s impressive relative gains might be challenging.

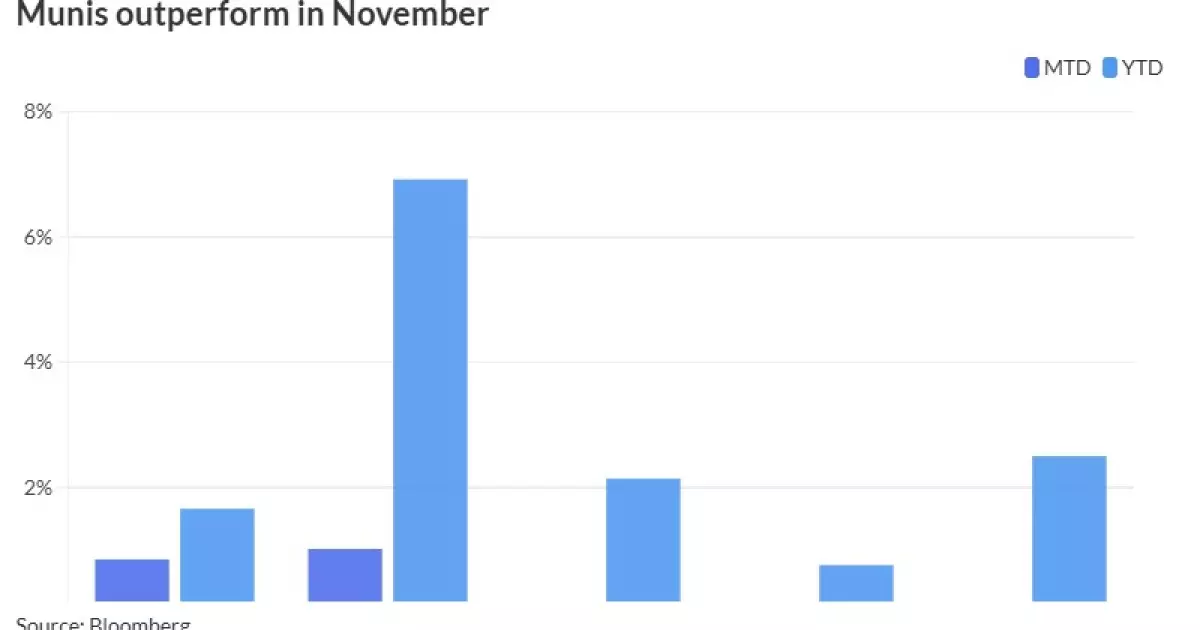

Performance data for municipals in November reflected an overall return of 0.85%, while year-to-date metrics stand at an impressive 1.66% according to Bloomberg’s Municipal Index. High-yield municipals, despite their more volatile nature, have also yielded positive returns throughout the month. Nevertheless, taxable municipals are showing slight losses, which underscores the mixed sentiment surrounding this segment of the market.

The economic backdrop remains critical as investors analyze potential macroeconomic indicators. Foux indicates that core Personal Consumption Expenditures (PCE) data will be closely observed, with implications for Federal Reserve monetary policy. Currently, discussions include conjectures for a 25 basis point rate cut, although the probability of this outcome remains uncertain.

Reports indicate robust economic performance in Q3, yielding forecasts for Q3 2024 GDP growth at 2.8%. Despite this, both DeGroot and Foux maintain a cautious outlook heading into 2025, suggesting that market conditions may not be overly favorable in the face of elevated valuations.

Despite the respectable performance of municipals thus far, challenges loom ahead. The historical strength of municipal performance in December—especially for high-grade bonds—encourages optimism; however, external market factors and valuation concerns temper expectations.

The final months of the year traditionally see a surge in municipal bond purchases, particularly following presidential election years. Therefore, while the outlook remains cautiously optimistic, it is accompanied by reminders of the market’s inherent volatility and the necessity for investors to remain vigilant as they navigate through the complexities of 2025’s financial landscape. The combination of attractive absolute yields, coupled with a favorable net-supply backdrop, presents a unique opportunity for municipal investors, albeit with a demand for careful assessment and strategic planning.