In the ever-evolving landscape of municipal bonds, recent activities have revealed a nuanced and complex interplay with U.S. Treasuries and equity markets. The recent trading session saw a mixed performance among municipal bonds as yields nudged slightly higher, influenced predominantly by fluctuations in the Treasury market.

The recent trading week has encapsulated a degree of volatility reminiscent of key historical moments in the markets. Municipal bond yields experienced minor adjustments, seeing rises of up to three basis points across various maturities. This consolidative behavior follows a period of increased turbulence following election outcomes, signaling that stakeholders are still navigating through a fog of uncertainty regarding future federal monetary policy. BlackRock strategists have projected that this volatility is expected to persist in the near term as market participants adjust their positions based on clearer insights into the ramifications of recent elections and anticipated Federal Reserve actions.

However, the underlying sentiment remains positive, with expectations of a decline in new issuances as we approach year-end, which historically supports municipal bond performance. The supply dynamics, paired with seasonal factors, enhance the stability and attractiveness of the municipal investment arena.

Reflecting on trends from previous years, this month mirrors the conditions of November 2016, where a significant spike in generic municipal yields occurred—reported to range from 50 to 70 basis points then. Kim Olsan, a seasoned portfolio manager, noted that rising U.S. Treasury yields are beginning to impact the flow of municipal bonds. This is particularly evident in the 2026 to 2032 maturity span, where the scarcity of 3.00% handles is noteworthy. Recent MSRB statistics indicate that approximately 16% of secondary tax-exempt trading activity has transpired within this context, indicating a market attempting to recalibrate its expectations.

Significantly, ratios comparing municipal yields to their Treasury counterparts have shown a reduction—settling in the 60% range for shorter maturities. Such ratios serve as a barometer of relative value between the two asset classes, highlighting potential pressures faced by municipal bonds as they navigate competitive pricing from the broader fixed-income market.

The dynamics across the yield curve present compelling opportunities for investors. Olsan emphasizes that many bonds that fall under the pre-refunded category, particularly those maturing in 2025, maintain attractive yields nearing the 3.00% mark. This scenario is appealing as investors seek both income and security, especially as the curve offers varied concessions, with yields elevating from around 3.00% for 10-year bonds to nearly 3.75% for those with 20-year maturities.

Interestingly, a level of buyer caution persists amidst forecasts of increased supply toward the end of 2024. Historical issuance data suggests November and December could see average issuances of about $60 billion, with past anomalies raising numbers well above this figure. This context influences market sentiments, as prospective rate fluctuations may result in tempered demand for new issues.

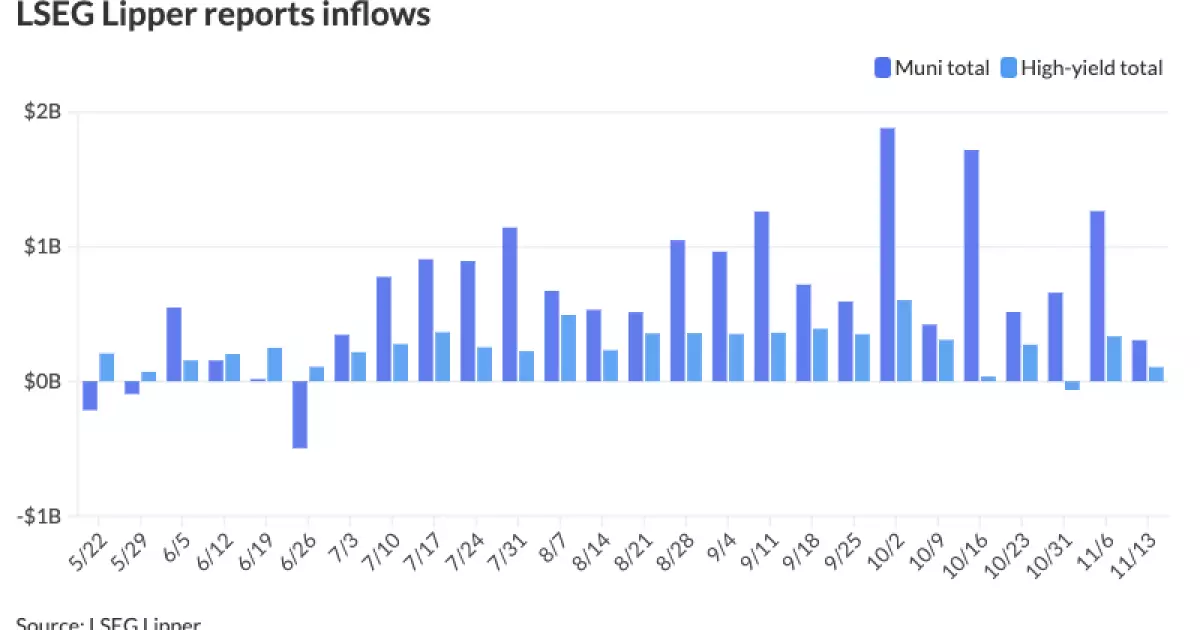

Furthermore, investor behaviors are evolving, signaling a shift toward more cautious stances. The last week reported a notable increase in inflows into municipal bond mutual funds, although slightly decreased compared to the previous week—marking a 20-week streak of consistent inflows. Comparatively, high-yield fund inflows also pick up, but the concurrent drop in support from fund-appetite could indicate potential yield pressures in the municipal market.

Turning to the primary market, a spectrum of new issuances demonstrates the ongoing demand for financing projects across various municipalities. High-profile transactions, such as those priced for the Los Angeles Department of Water and Power and the Omaha Public Power District, showcase that there is still robust appetite for well-structured municipal bonds.

As market participants prepare for year-end configurations and anticipate potential issuances, ongoing observations regarding bids wanted and fund flows become critical. The daily bid list remains relatively stable, which, while not alarming, may suggest underlying readiness for adjustments as year-end timelines converge.

Ultimately, while slight pressures in the short term seem imminent, the municipal market’s resilience, characterized by historical trends, appeals to long-term investors. The combination of controlled supply and attractive relative values positions municipal bonds as an enduring choice for those navigating a landscape marked by uncertainty and shifting economic indicators.