The municipal bond market showed signs of strength on Thursday, with firmer municipals following a robust U.S. Treasury session. Equities, however, closed with mixed results. Triple-A yields experienced a decline of one to five basis points, while USTs saw gains of seven to nine basis points. This movement led to a slight increase in muni to UST ratios, with various maturities displaying varying ratios at 3 p.m. EST.

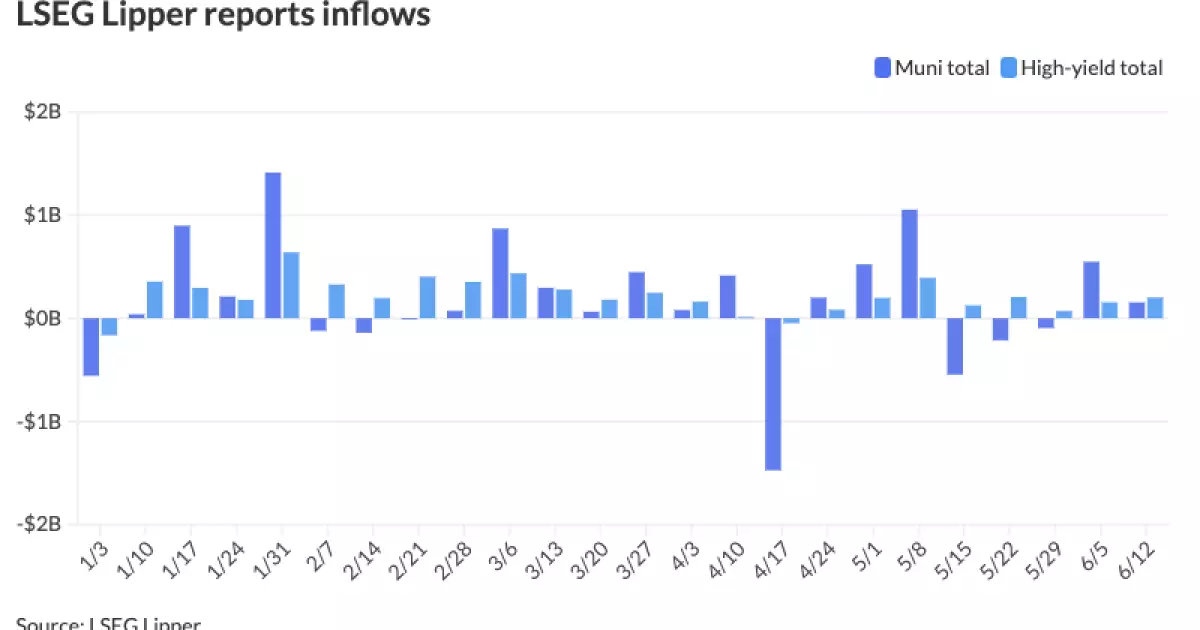

Although municipal bond mutual funds reported the second consecutive week of inflows, the base rates in the muni market have struggled to keep pace with the UST market rally. J.P. Morgan strategists noted that even after the recent rally, absolute yields appear attractive when compared to historical trading ranges. The long-term outlook for lower rates this year further supports the appeal of muni investments.

The gyrations in USTs based on economic data and FOMC communications pose challenges for municipals. Kim Olsan, senior vice president of municipal bond trading at FHN Financial, highlighted the upcoming $100 billion maturing or callable bonds, particularly within the June to August timeframe. While the supply increase is significant, it remains below the five-year monthly average.

High-yield continued to show strength in the market, with robust inflows reported after the previous week. The Bergen County Improvement Authority bonds, along with other GO offerings from states like California, Massachusetts, Washington, and Connecticut, saw tightening in prices, indicating strong demand from investors.

In the primary market, BofA Securities priced bonds for the Health, Education, and Housing Facility Board of the County of Shelby, Tennessee, while Denton, Texas, tapped the competitive market for GO refunding and improvement bonds. The pricing details and terms of these bonds demonstrate continued investor interest in municipal offerings.

Various municipal CUSIP request data highlighted an increase in volume, both month-over-month and year-over-year. The rise indicates growing interest in municipal bonds, with Texas leading the state-level request volume.

The AAA scales for municipals were adjusted, showcasing changes in yields across different maturities. Refinitiv MMD, ICE AAA, S&P Global Market Intelligence, and Bloomberg BVAL provided insights into the shifting landscape of municipal bond yields, with adjustments ranging from one to five basis points in various maturity terms.

Looking ahead, the recent market trends suggest ongoing investor appetite for municipal bonds, particularly in high-yield segments. The muni market’s ability to absorb fluctuations in USTs remains a key factor to watch, especially with the upcoming supply increase in the summer seasonals. The distribution of syndicate balances and price improvements in various maturities indicate a dynamic market environment where investors are actively seeking attractive yields.

Overall, the municipal bond market continues to offer opportunities for investors seeking stable income streams and potential capital appreciation. As interest rates remain low and market uncertainties persist, municipals provide a viable option for portfolio diversification and risk management. Investors should carefully evaluate their investment objectives and risk tolerance when considering municipal bonds in the current market environment.