The municipal bond market showed stability on Tuesday as investors anticipated the upcoming Federal Open Market Committee meeting and Consumer Price Index report. This was accompanied by a decline in U.S. Treasury yields and mixed performance in the equity markets towards the end of trading. Vikram Rai, head of municipal markets strategy at Wells Fargo, highlighted the significant adjustments that market expectations have undergone since the beginning of the year. Although economic data has been better than expected, leading to higher rates across the curve, investors are now realizing that the catalysts for further rate hikes may not be as strong as initially anticipated. The market is pricing in only one rate cut for the year, indicating that the hurdle for the Fed to lower rates is high.

Impacts of FOMC Meeting and CPI Report

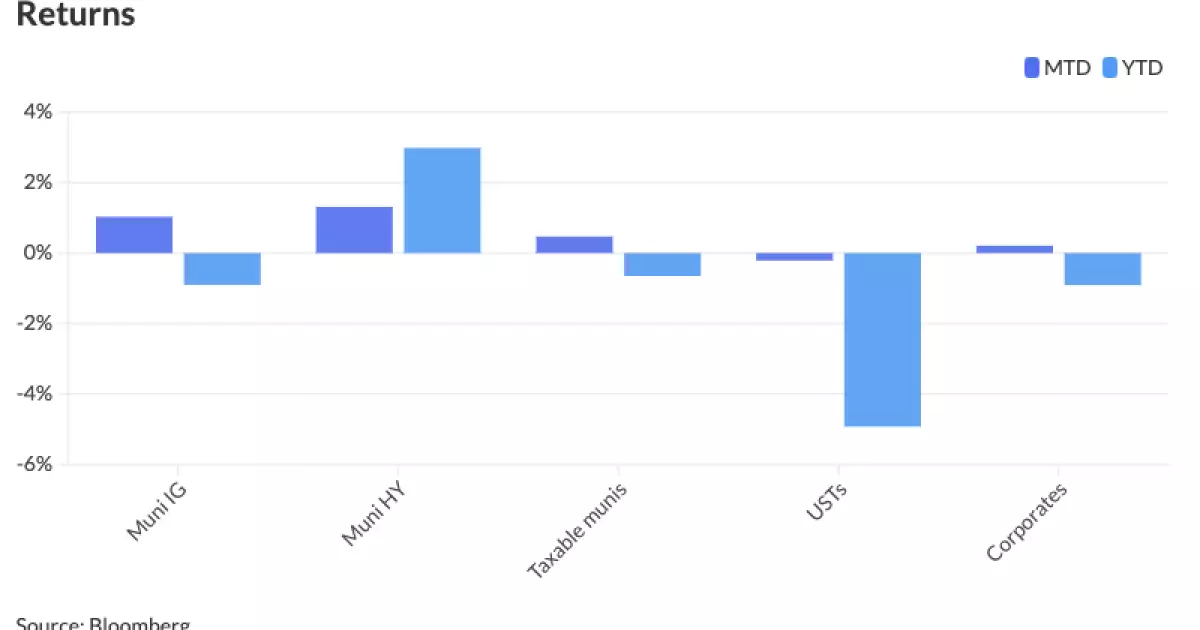

With the FOMC meeting and CPI report on the horizon, there is speculation that if inflation comes in below expectations or if the Fed adopts a more dovish stance, there could be a significant drop in yields. Despite the recent decline in muni-UST ratios following the UST selloff, Rai believes that valuations remain compelling. The ratios as of the latest data show that municipal bonds are still attractive relative to Treasuries, indicating potential opportunities in the market. However, caution is advised until the outcomes of the FOMC meeting and CPI report are known to prevent any adverse market reactions that could trigger sell-offs or sharp rallies.

Tuesday witnessed a flurry of activities in the primary market as various issuers tapped into the market to raise funds. Major deals included Morgan Stanley pricing $700 million of Los Angeles County tax and revenue anticipation notes, Barclays pricing $446.2 million of green general revenue bonds for the Massachusetts Water Resources Authority, and Morgan Stanley pricing $440.385 million of sustainable development multi-family housing revenue bonds for the New York City Housing Development Corp. The market also saw offerings from other entities like the Mobile County Industrial Development Authority, Michigan State University Board of Trustees, Maryland Economic Development Corporation, Connecticut Health and Educational Facilities Authority, and the New Mexico Finance Authority.

Despite a drop in overall supply, the forward supply calendar remains elevated compared to seasonal averages. Price resilience in the municipal market can be attributed to tax-exempt paper being attractively priced with nominal yields available. Furthermore, a massive seasonal reinvestment is underway, with $107 billion in tax-exempt principal maturing between June and August. This has led to a surge in net customer buying, indicating robust demand. Fund flows have been strong, with reinvestors temporarily holding funds in money market accounts. As a result, SIFMA rates have fallen below 3% for the first time in months.

Various sources provide slightly different yield curve data for municipal bonds and U.S. Treasuries. Refinitiv MMD, ICE AAA, S&P Global Market Intelligence, and Bloomberg BVAL each have their respective yield curve figures for different maturities. Treasuries showed firmer yields across the board at the close of trading, with a slight decline observed in most tenors.

The municipal bond market continues to navigate through evolving economic conditions and investor expectations. The upcoming FOMC meeting and CPI report are likely to shape market sentiment in the near term. With caution advised amidst market uncertainty, opportunities for investors may arise as the supply-demand dynamics and yield curve trends unfold.